What is Cash Flow Statement?

A cash flow statement is a financial statement that traces the flow of funds (or working capital) into and out of your business/company during an accounting period.

The cash flow statement’s primary purpose is to provide information regarding a company’s cash receipts and cash payments. The statement complements the income statement and balance sheet. It is important to note, cash flow is not the same as net income.

Cash flow is the movement of money into and out of your company, and it can be affected by several noncash transactions.

Table of Contents

Meaning of Cash Flow Statement

Cash flow statement is a statement of inflow or outflow of cash or cash equivalent of the company in the specified period. In other words, cash flow statement present the reason of changes in cash passion in two Balance Sheet date.

Cash flow includes inflow or outflow of cash or cash equivalent. It’s means, the movement of cash into the company and out of the company.

Hear ‘cash’ include cash in hand and cash at bank and ‘cash equivalent’ include short term investment that are quickly converted into cash. Information about inflow of cash or sources of cash and outflow of cash or application of cash are required for cash flow statement.

According to Accounting Standard, 3 cash flow statement is classified into the following three categories of cash inflow or outflow:

- Cash Flow from Operating Activities

- Cash Flow from Investing Activities

- Cash Flow from Financial Activities

Objectives of Cash Flow Statement

The main objective of cash flow statement are:

- To provide information on a firms liquidity and solvency to change cash flow in future circumstances.

- To provide additional information for evaluating changes in assets, liabilities and equity.

- To improve the comparability of different firms’ operating performance by eliminating the effects of different accounting methods.

- To indicate the amount, timing and probability of future cash flows

Importance of Cash Flow Statement

Following are the importance of cash flow statement:

- Cash flow statement helps to identify the sources from where cash inflows have arisen and where in the cash was utilized within a particular period.

- Cash flow statement is significant to management for proper cash planning and maintaining a proper matching between cash inflows and outflows

- Cash flow statement shows efficiency of a firm in generating cash inflows from its regular operations

- Cash flow statement reports the amount of cash used during the period in various long-term investing activities, such as purchase of fixed assets

- Cash flow statement reports the amount of cash received during the period through various financing activities, such as issue of shares, debentures and raising long-term loan

- Cash flow statement helps for appraisal of various capital investment programmes to determine their profitability and viability

- Cash flow statement helps the investors to judge whether the company is financially sound or not.

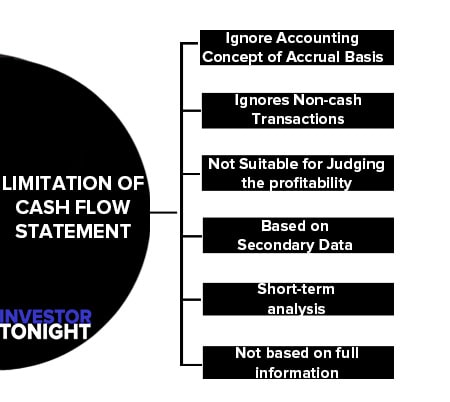

Limitation of Cash Flow Statement

Despite a number of uses, Cash Flow Statement suffers from the following limitations:

- Ignore Accounting Concept of Accrual Basis

- Ignores Non-cash Transactions

- Not Suitable for Judging the profitability

- Based on Secondary Data

- Short-term analysis

- Not based on full information

Ignore Accounting Concept of Accrual Basis

As CFS is based on cash basis of accounting, it ignores the basic accounting concept of accrual basis.

Ignores Non-cash Transactions

CFS ignores the non-cash transactions. In other words, it does not consider those transactions which do not affect the cash e.g., issue of shares against the purchase of fixed assets, conversion of debentures into equity shares, etc

Not Suitable for Judging the profitability

CFS is not suitable for judging the profitability of a firm as non-cash charges are ignored while calculating cash flows from operating activities.

Based on Secondary Data

CFS is based on secondary data. It merely rearranges the primary data already appearing in other statements i.e., Balance Sheet and Income Statement.

Short-term analysis

CFS is a technique of short-term financial analysis. It does not help much in knowing the long-term financial position.

Not based on full information

CFS does not present true picture of the liquidity of a firm. Liquidity does not depend upon ‘cash’ alone. Liquidity, also affected by the assets which can be easily converted into cash. Exclusion of these assets obstruct the true reporting of the ability of the firm to meet its liabilities

By itself, it cannot provide a complete analysis of the financial position of the firm.

It can be interpreted only when it is in confirmation with other financial statements and other analytical tools like ratio analysis.

Difference Between Funds and Cash Flow Statement

Funds flow and cash flow statements both are used in analysis of business transactions particular period. But there are some differences between these two statements which are given below:

- Funds flow statements is based on the accrual accounting system but in case of cash flow statements only those transactions are taken into consideration which affecting the cash or cash equivalents only.

- Funds flow statement analysis the sources and application of funds of long-term nature and the net increase or decrease in long-term funds will be reflected on the working capital of the firm.

The cash flow statement will only consider the increase or decrease in current assets and current’ liabilities in calculating the cash flow of funds from operations. - Funds Flow analysis is more useful for long range financial planning while

cash flow analysis is more useful for identifying and correcting die current liquidity problems of the firm. - Funds flow statement analysis is a broader concept, it takes into account both long-term and short-term funds into account in analysis.

But cash flow statement deals with the one of the current assets on balance sheet assets side only. - Funds flow statement tallies the funds generated from various sources with various uses to which they are put.

Cash flow statements start with the opening balance of cash and reach to the closing balance of cash by proceeding through sources and uses.

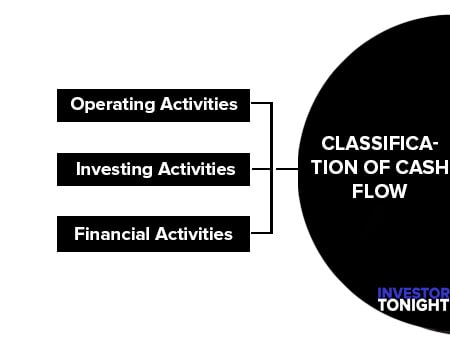

Classification of Cash Flow

Cash flow includes inflow or outflow of cash or cash equivalent. It means the movement of cash into the company and out of the company.

Cash flows can be classified into the following three categories:

Cash Flow from Operating Activities

Operation activities include those activities from which business income are generated and these are not investing or financing activities. Operation activities are result of the net profit or loss of the organisation.

For example cash receipts from sales of goods and rendering of services, royalties, fees, commission and other receiving. And cash payment to supplier of goods and provider of services, to employees and to other in behalf of employees and for revenue expenses.

Operating activities include the production, sales and delivery of the company’s product as well as collecting payment from its customers. This could include purchasing raw materials, building inventory, advertising and shipping the product etc.

Cash flows from operating activities generally result from the transactions and other events that enter into the determination of net profit or loss.

Examples of cash flows from operating activities are:

- Cash receipts from the sale of goods and the rendering of services;

- Cash receipts from royalties, fees, commissions and other revenue;

- Cash payments to suppliers for goods and services;

- Cash payments to and on behalf of employees;

- Cash receipts and cash payments of an insurance enterprise for premiums and claims, annuities and other policy benefits;

- Cash payments or refunds of income taxes unless they can be specifically identified with financing and investing activities; and

- Cash receipts and payments relating to futures contracts, forward contracts, option contracts and swap contracts when the contracts are held for dealing or trading purposes.

Cash Flow from Investing Activities

The separate disclosure of cash flows arising from investing activities is important because the cash flows represent the extent to which expenditures have been made for resources intended to generate future income and cash flows.

Examples of cash flows arising from investing activities are

- Cash payments to acquire fixed assets (including intangibles);

- Cash receipts from disposal of fixed assets (including intangibles);

- Cash payments to acquire investments in shares, warrants or debt instruments of other enterprises;

- Cash payments to disposal of investments in shares, warrants or debt instruments of other enterprises;

- Cash advances and loans made to third parties;

- Cash receipts from the repayment of advances and loans made to third parties;

Cash Flow from Financial Activities

The separate disclosure of cash flows arising from financing activities is important because it is useful in predicting claims on future cash flows by providers of funds (both capital and borrowings) to the enterprise.

Examples of cash flows arising from financing activities are:

- Cash receipts from issuing shares;

- Cash proceeds from issuing debentures, loans, notes, bonds, and other short or long-term borrowings; and

- Cash payment on redemption of preference shares or debentures;

- Cash repayments of amounts borrowed.

Read More Articles

- What is Financial Management?

- What is Financial Statements?

- What is Financial Statement Analysis?

- What is Ratio Analysis?

- What is Funds Flow Statement?

- What is Cash Flow Statement?

- What is Working Capital?

- What is Cost of Capital?

- What is Capital Budgeting?

- What is Dividend Policy?

- What is Cash Management?

- What is Depository?

- What is Insurance?

- What is Financial System?

- International Financial Reporting Standards

- Stability of Dividends

- What is Factoring?

- Determinants of Working Capital

- Public Finance

- Public Expenditure

- What is Public Debt?

- Classification of Public Debt

- Federal Finance

- Effect of Public Debt

- Expenditure Cycle