What is Cost Accounting?

Cost Accounting is defined as the process of accounting for cost which begins with the recording of income and expenditure or the bases on which they are calculated and ends with the preparation of periodical statements and reports for ascertaining and controlling costs.

Table of Contents

Cost Accounting Definition

Charles T. Horngren define Cost accounting is a quantitative method that accumulates, classifies, summarizes and interprets information for three major purposes: (i) Operational planning and control ;( ii) Special decision; and (iii) Product decision.

“Cost accounting is the process of accounting for costs from the point at which the expenditure is incurred of committed to the establishment of its ultimate relationship with cost units. In its widest sense, it embraces the preparation of statistical data, the application of cost control methods and the ascertainment of the profitability of the activities carried out or planned is defined as the application of accounting and costing principles, methods and techniques in the ascertainment of costs and the analysis of saving and/or excess as compared with previous experience or with standards.” – Institute of Cost and Management Accountants of London

“Cost accounting is defined as the application of costing and cost accounting principles, methods and techniques to the science, art and practice of cost control and the ascertainment of profitability. It includes the presentation of information derived therefore for the purposes of managerial decision making.” – Wheldon

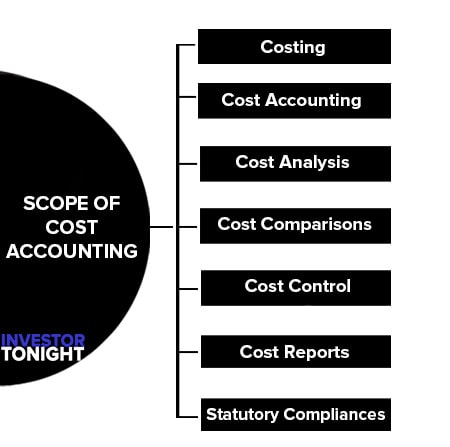

Scope of Cost Accounting

Cost accounting is a practice of cost control which is as follows:-

- Cost accounting is a branch of systematic knowledge that is a discipline by itself. It consist its own principles, concepts and conventions which may vary from industry to industry.

- Cost accounting is a science and arts both. It is science because it is a body of systematic knowledge relating to a wide variety of subject and an art because without the efficiency and experience of cost auditor it is not possible to use costing techniques efficiently.

Scope of cost accounting consists of the following functions:

- Costing

- Cost Accounting

- Cost Analysis

- Cost Comparisons

- Cost Control

- Cost Reports

- Statutory Compliances

Costing

Costing is the technique and process of ascertaining costs of products or services. The cost ascertainment procedure is governed by some cost accounting principles and rules. Generally, cost is ascertained using historical costs, standard costs, process cost, operation cost etc.

Cost Accounting

This is a process of accounting for cost which begins with the recording of expenditure and ends with the preparation of periodical statement and reports for ascertaining and controlling cost. Cost Accounting is a formal mechanism of cost ascertainment.

Cost Analysis

It involves the process of finding out the factors responsible for variance in actual costs from the budgeted costs and accordingly fixation of responsibility for cost differences. This also helps in taking better cost management and strategic decisions.

Cost Comparisons

Cost accounting also includes comparisons of cost involved in alternative courses of action such as use of different technology for production, cost of making different products and activities, and cost of same product/ service over a period of time.

Cost Control

It involves a detailed examination of each cost in the light of advantage received from the incurrence of the cost. Thus, we can state that cost is analyzed to know whether cost is not exceeding its budgeted cost and whether further cost reduction is possible or not.

Cost Reports

This is the ultimate function of cost accounting. These reports are primarily prepared for use by the management at different levels. Cost Reports helps in planning and control, performance appraisal and managerial decision making.

Statutory Compliances

Maintaining cost accounting records as per the rules prescribed by the statute to maintain cost records relating to utilization of materials, labour and other items of cost as applicable to the production of goods or provision of services as provided in the Act and these rules.

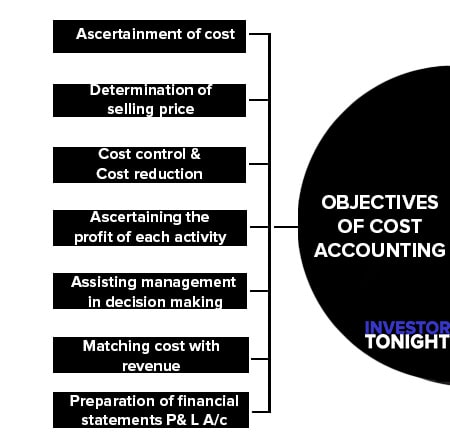

Objectives of Cost Accounting

The main objectives of cost accounting are as follows:

- Ascertainment of cost

- Determination of selling price

- Cost control & Cost reduction

- Ascertaining the profit of each activity

- Assisting management in decision making

- Matching cost with revenue

- Preparation of financial statements P& L A/c and Balance Sheet

Ascertainment of cost

The primary objective of cost accounting is ascertainment of cost. It (enables) the management to ascertain the cost of product, job, contract, service or unit of production so as to develop cost standard.

Cost may be ascertained, under different circumstances using one or more types of costing principles – standard costing, marginal costing, uniform costing etc.

Determination of selling price

Cost data are useful in the determination of selling price or quotations.nThe price of a product consists of total cost and the margin required.

Cost account provide detailed information regarding total cost in the form of various components. They also provide information in terms of fixed cost and variable costs so that extent of price reduction to be done incase of intensive competition etc., can be decided.

Cost control & Cost reduction

A basic function of cost accounting is to control cost. The objective is to minimize the cost of manufacturing comparison of actual cost with standard reveals the discrepancy is variances.

If the variances are adverse, the management enters into investigation so as to adopt corrective action immediately.

Ascertaining the profit of each activity

The profit of any activity can be ascertained by matching cost with the revenue of that activity. The purpose under this step is to determine costing profit or loss of any activity on an objective basis.

Assisting management in decision making

Decision making means as a process of selecting a course of action out of two or more alternative courses. For making a choice between different courses of action.

It is necessary to make a comparison of the outcomes which may be arrived under different alternatives. Such comparison has only been made possible with the help of cost accounting information.

Cost accountings are helpful to the management in taking decision regarding:

- Production of discontinuation of a product.

- Utilization of idle capacity.

- The most profitable sales mix.

- Alternative based on key factor.

- Export decision.

- Make or Buy decisions etc.

Matching cost with revenue

The determination of profitability of each product, process, department etc. is the important object of costing.

Preparation of financial statements P& L A/c and Balance Sheet

To prepare these statements, the value of stock work in progress, finished goods etc. all essential In the absence of the costing department when we have to close the accounts it rather takes too much time.

But good system of costing facilitates the preparation of statements as the figures are easily available they can be prepared monthly or even weekly.

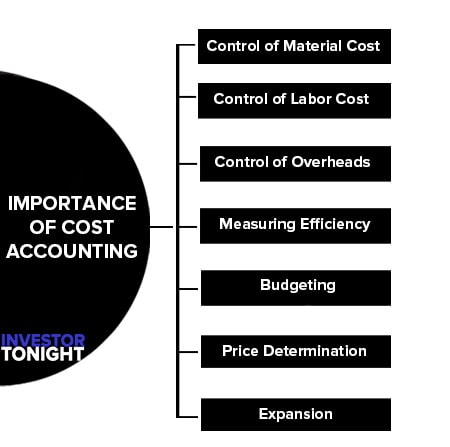

Importance of Cost Accounting

Following are the importance of cost accounting:

- Control of Material Cost

- Control of Labor Cost

- Control of Overheads

- Measuring Efficiency

- Budgeting

- Price Determination

- Expansion

Control of Material Cost

Cost of material is a major portion of the total cost of a product. It can be controlled by regular supply of material and spares for production, maintaining optimum level of funds in stocks of materials and stores.

Control of Labor Cost

If workers complete their work within the specified time cost of labour can be controlled.

Control of Overheads

By keeping a strict check over various overheads such as factory, administrative and selling & distribution, this can be controlled.

Measuring Efficiency

Cost accounting provides information regarding standards and actual performance of the concern activity for measuring efficiency.

Budgeting

The preparation of the budget is the function of costing department and budgeting is done to ensure that the practicable course of action can be chalked out and the actual perform corresponds with the estimated or budgeted performance.

Price Determination

On behalf of cost accounting information, management is enable to fix remunerative selling price for various items of products and services in different circumstances.

Expansion

The management may be able to formulate its approach to expansion on the basis of estimates of production of various levels.

Advantages of Cost Accounting

Following are the advantages of cost accounting:

- Advantages to the management

- Advantages to the Employees

- Advantages to the Creditors

- Advantage to the Government

- Advantage to the public

Advantages to the management

- Facilitates planning

- Helps in formulating policies

- Useful in setting up objectives and standards of performance

- Facilitates cost comparison

- Leads to effective cost control

- Determines the selling price

- Ascertains profit of each activity

- Assists the Management in decision making

- Facilitates cost reduction

- Measures performance.

Advantages to the Employees

- Ensures fair incentive wage schemes

- Facilitates job security, recognition and promotion

- Useful in measuring operating efficiency of the employees

Advantages to the Creditors

Measures the financial strength and creditworthiness of the business. 2) Attract investors for extending their credit facilities. 3) Creates trustworthiness among the creditors, debenture holders, banks etc.

Advantage to the Government

- It helps to formulate business policies and national plans for industrial development.

- It facilitates assessment of taxation, and establishment of indexes.

- It assists in effective utilization of resources, i.e. materials, labor and machines etc.

- It assists the government for cost reduction, price fixation, export and import and granting subsidy etc.

Advantage to the public

- It helps in elimination of wastages and inefficiencies.

- It facilitates the consumers to pay fair price for products.

- It leads to progress of national economic growth.

- Creates employment opportunities.

- Increases the living standards of the people.

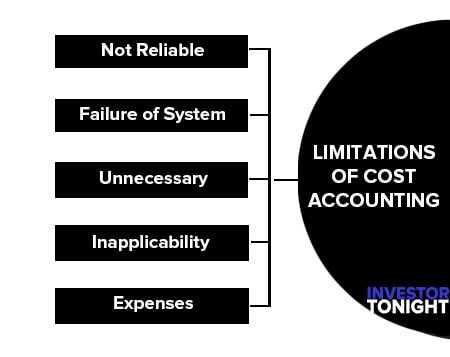

Limitations of Cost Accounting

These are the following limitations of cost accounting:

Not Reliable

Cost Accounting is based on estimates and so it is not reliable.

Failure of the System

Cost Accounting system has failed to produce desired results in many concerns. Thus it could be said that this system is at fault.

Unnecessary

It is not necessary in Business concern as it involves duplication of work.

Inapplicability

Modern methods of cost accounting are not applicable to every type of industries.

Expenses

It is expensive because double set of account books has to be maintained and its introduction involves considerable amount of expenditure.

Read More Articles