What is Cash Management?

Cash Management is a technique to plan and control of cash in such a way that sufficient cash is always available to meet the obligations of the firms and excess balances, if any, may invested to enhance profitability.

A cash management scheme therefore, is a delicate balance between the twin objectives of liquidity and costs.

Table of Contents

Objectives of Cash Management

The main objective of cash management is to trade-off liquidity and profitability in order to maximise the firms value. The larger the cash balance, the greater the degree of liquidity, the lesser will be profit earning capacity of the firm.

Similarly, the lesser the cash balance and the degree of liquidity, the more will be the profit earning capacity. So every firm needs optimum level of cash.

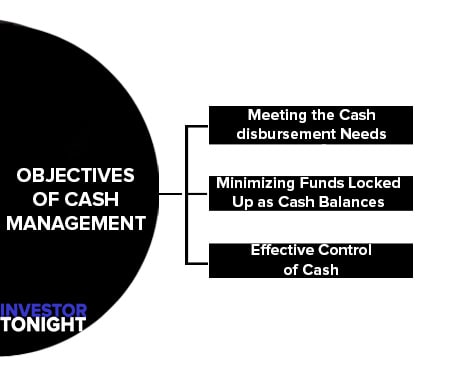

The basic objectives of cash management are

- Meeting the Cash disbursement Needs

- Minimizing Funds Locked Up as Cash Balances

- Effective Control of Cash

These are conflicting and mutual contradictory and the task of cash management is to reconcile them.

Meeting the Cash disbursement Needs

In the normal course of business firms need cash to invest in inventory, pay to short term lenders and to make payment for operating expenses. If these payment are not meet on time, the business operations may be disturbed.

Thus it is needless to say that all the business activities would remain stand still if proper payment schedule is not maintained. The primary objectives of cash management is to ensure the meeting of cash outflows or disbursements as and when required.

Minimizing Funds Locked Up as Cash Balances

Another objectives of cash management is to minimise the amount locked up as cash balance because whatever cash balance is maintained, the firm looses interest income on that balance. Therefore, investment in idle cash balance must be reduced to minimum.

Effective Control of Cash

Usually, the financial manager is confronted with two conflicting views. On one hand, although the higher cash balance ensures proper payment which will prevent the firm from bankruptcy or insolvency, will make good relations with suppliers, firms can bargain for discount, but it also implies that large funds will remain idle as cash is a non earning asset and the firm will have to forgo profits.

On the other hand, if a firm keeps its cash balance at low level, it cannot meet its payment schedule. The aim of cash management should be to try to have an optimum level of cash by taking into account the above facts.

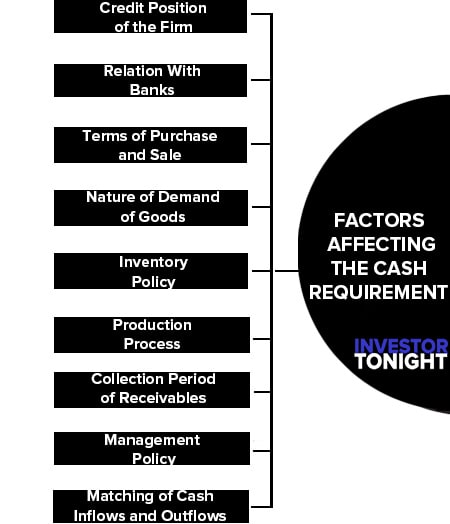

Factors Affecting the Cash Requirement

A firm must have so much of cash balance, that daily requirements and unexpected demands can be met out. The factors affecting cash requirements and their effect on cash management are as follows:

- Credit Position of the Firm

- Relation With Banks

- Terms of Purchase and Sale

- Nature of Demand of Goods

- Inventory Policy

- Production Process

- Collection Period of Receivables

- Management Policy

- Matching of Cash Inflows and Outflows

Credit Position of the Firm

Firms with good and sound credit standing and goodwill need not to maintain separate cash for unforeseen situations, as cash is available to such firms whenever needed. They can get liberal credit facilities to purchase necessary material. On the contrary, firms with bad credit position shall have to maintain high level of cash balance.

Relation With Banks

If firm has good relation with banks, it can get the facility of cash credit and bank overdraft resulting less requirement of maintaining cash balance.

Terms of Purchase and Sale

Terms of purchase and sale also affect the level of cash balance. If a firm has facilities to buy material on credit terms but sells its products on cash, it can operate its business affairs with a little cash balance.

On the other hand, if the firm makes purchases on cash basis but sells its products to customers on credit terms, larger cash balance will have to be maintained.

Nature of Demand of Goods

If there is a steady demand of product in the market i.e. products of day to day requirement (necessary items) and the product is sold for cash or for short credit period, firm will need low level of cash. On the contrary, firm’s engaged in the production of luxury items have to maintain high level of cash.

Inventory Policy

If high level of inventory is maintained by the firm, large amount is required for this, while if a firm follows just in time inventory system, it need not to maintain large cash funds.

Production Process

Longer the production process, higher the requirement of cash balance but if production process is short, the need of maintaining cash balance will be low.

Collection Period of Receivables

If, in a firm, speed of collection of accounts receivable is quick, the cash will be available at all time, bad debts will be lower and, the firm is not required to carry large cash balance. However, if collection period is large, high balance will have to be maintained.

Management Policy

Cash balance held by a firm also depends upon management policies and attitude towards the liquidity preference, risk bearing capacity, sales and purchases policy, quantity of investment and inventory etc. If the owners and managers of the firm want strict plans of cash management, it can work with lower cash balance otherwise high balance will be required.

Matching of Cash Inflows and Outflows

The extent of non synchronization between cash inflow and outflow determines the requirement of cash . Higher the degree of variance between cash collection and disbursement, higher will be the requirement of cash and vice versa.

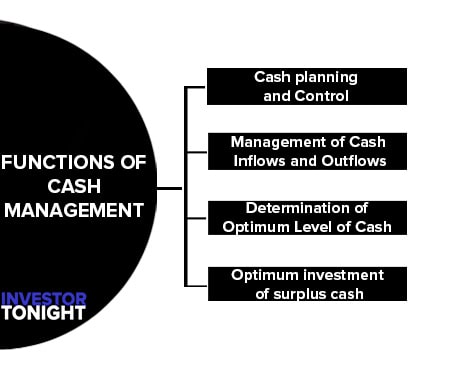

Functions of Cash Management

Management of cash is an important function of the finance manager. He should formulate strategies for the following areas:

- Cash planning and Control

- Management of Cash Inflows and Outflows

- Determination of Optimum Level of Cash

- Optimum investment of surplus cash

Cash planning and Control

Cash planning is a process of predicting cash inflows and cash outflows of the firm so as to determine surplus or shortage of cash. At times, a firm can have idle cash with it if its cash inflows are more than its outflows.

Such excess can be anticipated and properly invested if cash planning is resorted to. Similarly, cash poor position can be corrected if the cash needs are planned in advance.

Thus, cash planning is a technique to plan and control the use of cash. This may be done on daily, weekly or monthly basis depending upon the size of the firm and policies of management. Cash budget is the most significant tool for cash planning and control.

- Cash Budget: A firm should hold adequate cash balances but should avoid excessive balances. The firms has therefore to assess its need for cash properly. “A cash budget is a statement showing anticipated cash inflow, outflow and net cash balance for a future period of time”.

Cash budget is an important device to forecast the predictable discrepencies between cash inflows and outflows over a projected time period. It is a summary statement which shows the estimated cash inflows and cash outflows over the firms planning horizon.

The time period for which cash budget can be prepared depends upon the following points

- Impact of seasonal variations on cash flows

- Degree and pattern of fluctuations in cash flows

- Preciseness in prediction of cash flows.

A Cash Budget has the following benefits:

- It coordinates the timings of cash needs. It identifies the period(s) when there might either be a shortage of cash or remain an abnormally large balance.

- It also helps to pinpoint period(s) when there is likely to be excess cash to take advantage like cash discounts on its accounts payable, capital expenditure decision etc.

- Lastly it helps to plan/arrange adequately needed funds (avoiding excess/shortage of cash) on favorable terms.

There are three methods to prepare the cash budget:

- Receipt and Payment Method

- Adjusted Profit and Loss Account Method

- Projected Balance Sheet Method

For short term (monthly, weekly, quarterly) cash budget, receipt and payment method is used while for long term cash budget other methods can be used.

With advance planning through cash budget firms get adequate time to take the necessary action for borrowing and lending of cash on the terms which are most advantageous to the firm.

- Cash Flow Analysis: A simple definition of a cash flow statement is – ‘a statement which discloses the causes of changes in cash position between the two periods’.

As per ICWAI, “Cash flow statement is a statement setting out the flow of cash under different heads of sources and their utilizations to determine the requirements of cash during the given period and to prepare for its adequate provisions”.

Thus along with changes in the cash position the cash flow statement also outlines the reasons for such inflows or outflows of cash which in turn helps to analyze the functioning of the business.

Cash flow analysis is based on historical data while cash budget is a technique for future estimation. - Ratio Analysis: Ratios like cash turnover ratio, cash flow coverage ratio, cash payment ratio are also important techniques of cash planning and control.

Management of Cash Inflows and Outflows

After knowing the cash position with the help of cash budget, the management should work out the basic strategies to be employed to manage its cash flows. So that there does not exist a significant deviation between projected cash flows and actual cash flows.

In the words of Van Horne, “Optimising cash availability involves accelerating collections as much as possible and delaying payments as long as is realistically possible”. The methods used for accelerating the collections and decelerating disbursements are as follows –

- Accelerating Cash Collections: In order to accelerate cash inflows, the collection from customers should be prompt. The finance manager has to devise action not only to fraudelent diversion of cash but also to speed up collection of cash.

A firm can conserve cash and reduce its requirements for cash balances if it can speed up its cash collections by issuing invoices quickly or by reducing the time lag between a customer pays bill and the cheque is collected and funds become available for the firm’s use i.e. first of all customers should be encouraged to make the payments as early as possible and secondly efforts should be made to quickly process and collect the cheques and drafts deposited by the customers.

There are basically three types of floats that create the difference

- Mail Float: The time gap between the postage of cheques / drafts by the debtors and the receipt of the same in the firm is called mail or postal float.

- Processing Float: Time taken in processing the cheque within the firm before they are deposited in the bank due to lethargy of employees is termed as processing float.

- Collection Float: The time difference between the cheque is deposited into the bank and its actual realisation is called collection float.

Decentralised collection systems known as concentration banking and lock box systems can help us to speed up collection of cash and in reducing the time involved in these floats considerably.

- Concentration Banking: A large firm operating over wide geographical areas can speed up its collection by following a decentralised collection procedure.

In concentration banking the company establishes a number of strategic collection centres in different regions instead of a single collection centre at the head office.

Payments received by the different collection centres are deposited with their respective local banks which in turn transfer all surplus funds to the concentration bank of head office. - Concentration banking is one important and popular way of reducing the size of the float as it helps in:

- Reduction of Mailing Time: Under the system of concentration banking, as the collection centres themselves collect cheques from the customers and immediately deposit them in local bank account, the mailing time is reduced. If collection centres are allowed to send bills to the customers of their respective areas, the time required for mailing is less than the bills are mailed from the head office.

- Reduction of Time Required to Collect Cheques: As the cheques deposited in the local bank accounts are usually drawn on banks in that area, the average collection period also comes down.

- Expediting Collection of Cash: The system of concentration banking also helps in quicker collection of cash as it reduces the size of deposit float.

- Reduction of Mailing Time: Under the system of concentration banking, as the collection centres themselves collect cheques from the customers and immediately deposit them in local bank account, the mailing time is reduced. If collection centres are allowed to send bills to the customers of their respective areas, the time required for mailing is less than the bills are mailed from the head office.

- Lock Box System: Lock-box system is another step in expediting collection of cash. Lock-Box is a post office box maintained by a firm’s bank that is used as a receiving point for customer remittance.

Collection centre and its actual depositing in the local bank account. Under lock-box system, the firm hires a post-office box and instructs its customers to mail their remittances to the box. - Minimum Number of Bank Accounts: Sometimes a firm may have more bank accounts and we know it is the policy of banks to have some specified minimum balance in the account, resulting blocking of some part of the cash in each such account.

- Slowing Disbursement: The operating cash requirement can be reduced by slow disbursement of accounts payables. Slow disbursements represent a source of funds requiring no interest payments. But this should not impair the credit rating or reputation of the firm.

There are several techniques to delay payment of accounts payable.

Some of important method are as below:

- Centralised Disbursement Centre: The firm should follow the centralised system for disbursements as against decentralised system for collections. Under centralised system, as all payments are made from a single control account, there will be delay in presentation of cheques for payment by parties who are away from the place of control account.

- Avoidance of Early Payments: According to the terms of credit, some credit period is allowed to the buyers. The finance manager should try to control over the timing of payments so as to ensure that bills are paid only as they become due.

- Playing the Float: It is a technical process by which a firm can make maximum utilisation of cash. Float means the amount blocked in cheques issued but yet to be collected and encashed. In other words, float is the difference between the balance shown in firm’s cash book (bank column) and balance in the pass book of the bank.

The difference between the total amount of cheques drawn on a bank account and the balance shown on the bank’s book is caused by transit and processing delay.

For example, If the party is at some distant station then cheque will come through post and it may take a longer period before it is presented.

If the finance manager can accurately estimate when the cheque issued will be deposited and collected, he can invest the ‘float’ during the float period to earn a return. However playing the float should not result into loss of credit worthiness of the firm.

- Centralised Disbursement Centre: The firm should follow the centralised system for disbursements as against decentralised system for collections. Under centralised system, as all payments are made from a single control account, there will be delay in presentation of cheques for payment by parties who are away from the place of control account.

Determination of Optimum Level of Cash

A business firm maintains the optimum cash balance for transaction and precautionary motives. This amount will depend on risk return trade off. When the firm runs out of cash or it has low liquidity, then it will have either to sell short-term securities or borrow cash. In both these situations, the firm has to bear transaction cost.

On the contrary, if firm maintains high level of cash balance, the opportunity to earn interest is lost. So, the potential interest lost on holding large cash balance involves opportunity cost to the firm. The optimal level of cash is determined by the trade-off between transaction cost and opportunity cost as shown in the following figure:

It is clear from the above diagram that if the firm maintains large cash balances, its transaction cost will decline but opportunity cost will increase or vice-versa. At point P the sum of the two costs i.e. total cost is the minimum. This is the point of optimal cash balance which a firm should seek to achieve.

Optimum investment of surplus cash

Cash kept by the firm in excess of its normal need is called the surplus cash. Due to changing working capital needs or unpredictable requirements the finance manager is required to consider the minimum cash balance that the firm should keep to avoid the cost of running out of funds. This minimum level may be termed as’Safety level of Cash’.

Formula’s used for this level are

- During Normal Periods: Safety level of cash = Desired days of cash x Average daily cash outflows.

- During Peak Periods: Safety level of cash = Desired days of cash at the peak period x Average of highest daily cash outflows

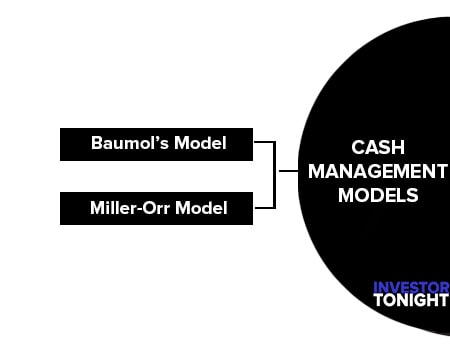

Cash Management Models

To help in determining optimum cash balance, several types of cash management models have been designed. Out of such models, two of them are:

- Baumol’s Model, i.e., optimum cash balance under certainty,

- Miller-Orr Model i.e., Optimum cash balance under uncertainty are quite popular.

Baumol’s Model

Baumol’s model, suggested by William J. Baumol, considers cash management similar to an inventory management problem. It is a formal approach in determining a firm’s optimum cash balance under certainty. According to this model, optimum cash level is that level of cash where the carrying costs and transactions costs are the minimum.

The carrying cost refers to the cost of holding cash (opportunity cost) namely, the interest foregone on marketable securities. The transaction cost refers to the cost involved in getting the marketable securities converted into cash. It can be understood by following diagram :

For preparing the above diagram it is assumed that the demand of cash is steady for a given period of time. During this period the firm can recover cash after selling the investments.

Suppose opening cash balance with firm is C and as and when this balance is spent on various expenses, the firm sells the investment hence when cash balance becomes zero, the funds are transferred from investment to cash.

This optimum cash balance according to this model will be at that point, where these two costs are minimum.

The formula for determining optimum cash balance is:

C = Optimum cash balance

U = Annual or monthly cash disbursement

P = Fixed cost per transaction

S = Opportunity cost of holding cash (one rupee p.a. or p.m.)

The Baumol’s model has the following assumptions:

- The firm can forecast its cash requirement with certainty.

- Cash disbursement will be steady during a given period.

- The sequence of cash receipt and disbursement will continue to be the same.

- Whenever the firm converts its securities into cash, its transaction cost will be the same.

- The firm’s opportunity cost of holding cash is known and it is the same over time.

Limitation of Baumol’s Model

The assumptions do not fit in practical environment. Practically cash disbursements are found to be variable and uncertain and variance will be there in cash receipts and disbursements during each month or days in a month. Transaction and opportunity cost also varies over time.

Miller-Orr Model

Miller-Orr (MO) Model helps in determining the optimum level of cash when the demand for cash is not steady and cannot be known in advance. MO model deals with cash management problem under the assumption of random cash flows by laying down control limits for cash balances.

Limitation of Miller-Orr Model

- Upper limit

- lower limit

- return point.

Setting of the control limits depend upon the fixed cost associated with a securities transaction, the opportunity cost of holding cash and the degree of likely fluctuations in cash balances. These limits satisfy the demands for cash at the lowest possible cost.

The following diagram illustrates the Miller-Orr Model:

The MO Model is more realistic as it allows variations in cash balance within lower and upper limits.

Recent developments in Cash Management: Both technological advancement and desire to reduce cost of operations has led to some innovative techniques in managing cash. Some of them are :

- Electronic Fund Transfer

- Zero Balance Account

- Petty Cash Imprest System

- Virtual Banking

Read More Articles

- What is Financial Management?

- What is Financial Statements?

- What is Financial Statement Analysis?

- What is Ratio Analysis?

- What is Funds Flow Statement?

- What is Cash Flow Statement?

- What is Working Capital?

- What is Cost of Capital?

- What is Capital Budgeting?

- What is Dividend Policy?

- What is Cash Management?

- What is Depository?

- What is Insurance?

- What is Financial System?

- International Financial Reporting Standards

- Stability of Dividends

- What is Factoring?

- Determinants of Working Capital

- Public Finance

- Public Expenditure

- What is Public Debt?

- Classification of Public Debt

- Federal Finance

- Effect of Public Debt

- Expenditure Cycle