What is Security?

The world security may be defined as, ‘an instrument of a promissory note or a method of borrowing or lending or a source of contributing to the funds needed by a corporate body or a non-corporate body.’

In a legal sense also security can be defined as, ‘inclusive of shares, scrips, stocks, bonds, debentures or any other marketable securities of like nature in or of any debentures of a company or a corporate body, government or semi-government body, etc.’

It includes all rights and interests, including warrants, loyalty coupons, etc. issued by any of the bodies organizations or the government.

Table of Contents

Security Definition

A simple definition of security is any proof of ownership or debit that has been assigned a value and may be sold. (Today, evidence of ownership is likely to be a computer file, while once it was a written piece of paper.) For the holder, security represents an investment as an owner, creditor or rights to ownership and which the person hopes to gain profit. Examples are stocks, bonds and options.

The securities and Exchange Act of 1934 provides the more complicated definitions. The term, security means any note, stock treasury stock, bond debenture certificate of interest or participation in any profit-sharing agreement or in any oil, gas or other mineral royalty or lease any collateral trust certificate, certificate of deposit, for security any put, call straddle option or privilege all any security, certificate of deposit or group or index of securities.

What is Valuation?

The process of determining the current worth of asset or company. There are many techniques that can be used to determine value, some are subjective are others are objectives.

In fences, valuation is the process of estimating what something is worth. Items that are usually valued are financial asset or liability. Valuation can be done on assets (for example, investments in market table security such as stock options, business enterprise or intangible asset such as patents and tread mark.) or in liabilities.

Valuations are needed for many reasons such as investment, analysis capital budgeting merger and acquisition transactions financial reporting, taxable events to determine the proper tax liability and in litigation.

Valuation of finance assets is done using one or more of these types of models:

- Absolute value model that determine the present value of an asset’s expected future cash flows: These kinds of models table two general from multi- period models such as discounted cash flow models or single period models such as the Gordon model. These models rely on mathematics rather than price observation.

- Relative value: Models determine value based on the observation of market price of similar assets.

- Option pricing model: Are used for certain type of financial assets warrants, put option call option, embedded option such as a callable option are a complex present value model .The most common option pricing models are the blank schools- Merton models and lattice value.

Concept of Value

The term value has been used to convey a variety of meanings. The different meanings of value are useful for different purposes. The various concepts of value are discussed below:

- Book value

- Market value

- Going Concern Value

- Liquidation Value

- Replacement Value

- True concept of value

Book value

Book value of security is an accounting concept. The book value of an equity share is equal to the net worth of the firm divided by the number of equity share, where the net worth is equal to equity capital pulse free reserves. The market value may fluctuate around the book value but may be higher if the future prospects are good

Market value

The market value of an asset or security is the value at which it can be sold at present. It is argued that actual market prices are appraisals of knowledgeable buyers and sellers who are willing to support their opinions with cash. Market price is a definite measure that can readily be applied to a particular situation and it minimizes the subjectivity of other methods in favour of a known yardstick of value.

Going Concern Value

In the valuation process, the valuation of shares in done on the going concern basis. In a going concern, we assess the value of an existing mixture of assets which provide a stream of income. The going concern value is the price which a firm could realise if it is sold as an operating business. The going concern value will always be higher than the liquidation value.

The difference between these two value will be due to value of organization, reputation etc. we may command goodwill if the concern is sold as a going concern.

For example, if the future maintainable profits of a firm are estimated to be Rs.5,00,000 per annum and the expected normal rate of return (capitalization rate)is 10%, the going concern value of the firm than would be: 5, 00,000 x100/10 = Rs.50, 00,000

Liquidation Value

If the assets are valued at their breakdown value in the market and take net fixed assets plus current assets minus current liabilities as if the company is liquidated, then divide this by the number of shares, the resultant value is the liquidating value per share. This is also an accounting concept.

Replacement Value

When the company is liquidated and its assets are to be replaced by new ones, their prices being higher, the replacement value of share will be different from the breakdown value some analysts take this replacement value to compare with the market price.

True concept of value

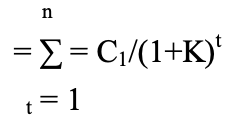

A business enterprise keeps or uses various assets because they generate cash inflows. Value is the function of cash inflows and their timing and risk. When cash inflows are discounted at the required rate of return to account for their timing and risk, be get the fair value or the present value of the asset. In financial decision making such as valuation securities, it is the present value concept which is relevant symbolically:

Vo = C1 /(1+K)1 + C2/(1+K)2 + C3/(1+K)3 +—- Cn/(1+k)n

Where,

Vo = Value of the asset at time zero

C1 , C2, C3 = Expected cash flow in period 1, 2, 3, and so on.

k = Discount rate applicable to cash flows.

n = Expected life of the asset.

t = Time period

Example

An investor who uses a 10 percent discount rate would value an asset that is expected to provide annual cash inflow of Rs. 1000 per year for the next ten years as being worth Rs. 6145, as calculated below:

V0 =∑ 1000/t = (ADF10% ADF10% , 10 year)

t =1(1.10)t

= 1000 *6.145

= Rs.6, 145

Read More Articles