What is Mutual Fund?

A Mutual fund is a trust that pools a number of savings investors, who shares a common financial goal.

From the aforesaid definition, we can understand the concept of Mutual fund and the key points as mentioned hereunder:

- Mutual fund is a trust

- Mutual fund pools money from a group of investors called Unit Holders

- The investors share common financial goals

- Invest the money, collected from small investors into securities (shares, bonds etc.,). It is called as diversified investment.

- Mutual Fund use professional expertise (investment management skills) on investments made.

- Asset classes of investments match the stated investment objectives of the scheme

- Incomes and Gains from the investments are passed on to the unit holders based on the proportion of the number of units they own.

Table of Contents

- 1 What is Mutual Fund?

- 2 Mutual Fund Definition

- 3 How does a Mutual Fund Work?

- 4 Types of Mutual Fund

- 5 Parties to Mutual Fund

- 6 Advantages of Mutual Funds

- 7 Disadvantages of Mutual Funds

- 8 SEBI Guideline of Mutual Fund : SEBI Regulation Act 1996

- 9 Mutual Fund Myths

- 10 Demat Account is Required for MF investments

- 11 Establish Your Financial Goals for Mutual Fund

Mutual Fund Definition

According to Encyclopedia Americana, “Mutual funds are open end investment companies that invest shareholders’ money in portfolio or securities. They are open ended in that they normally offer new shares to the public on a continuing basis and promise to redeem outstanding shares on any business day.”

According to Securities and Exchange Board of India Regulations, 1996 a mutual fund means “a fund established in the form of trust to raise money through the sale of units to the public or a section of the public under one or more schemes for investing in securities, including money market instruments”.

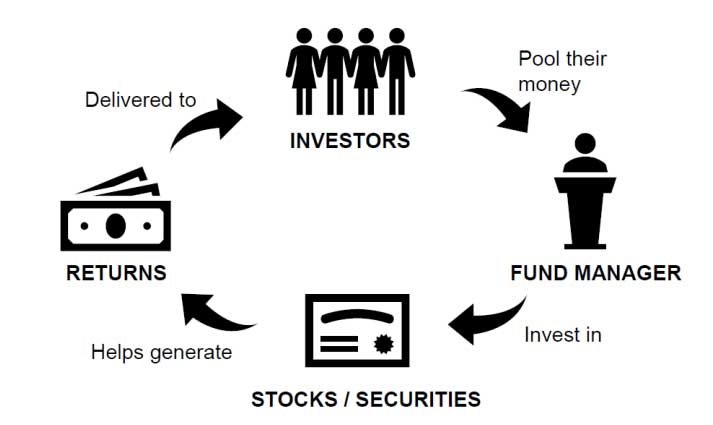

How does a Mutual Fund Work?

- Pool of investors money.

- Invested according to pre-specified investment objectives.

- Benefits accrue to those that contribute to this pool.

- There is thus mutuality in the contribution and the benefit.

- Hence the name ‘mutual’fund.

Types of Mutual Fund

Mutual funds could be classified in many ways based on structure, objectives of investment, pattern ‘of investments and returns, etc.

Based on Structure

Open Ended Funds

Under an open-ended scheme, the mutual fund will announce daily purchase and sales, price of the Units of the scheme. If you want to buy the Units today, you can buy the same at the sale price. Maybe, after six months, if you decide to sell the units, you can sell at the purchase price announced by the mutual fund on that date.

Thus, the mutual fund offers instant liquidity for your investment under the open-ended scheme by taking responsibility of purchasing back the Units. There is no limit to the size of the funds. Investors can invest as and when they like. The purchase price is determined on the basis of Net Asset Value (NAV). NAV is the market value of the fund’s assets divided by the number of outstanding Shares/Units of the fund.

An open-ended fund is one that is available for subscription all through the year. These do not have a fixed maturity. Investors can conveniently buy and sell units at Net Asset Value (“NAV”) related prices. The key feature of open-ended schemes is liquidity

Close Ended Funds

Under close-ended schemes, there is no repurchase facility. However, the Units are listed in the stock market and investors can sell and buy Units like any other securities in the market. The scheme has a specific life (say 10 years or 5 years) and at the end of the period, the mutual fund sells securities bought under the scheme and disburses the proceeds to Unitholders.

When the stock market was doing well, many of the schemes have attracted investors and there was also active secondary market. But they lost the fancy of the investors after couple of stock market failures.

Today, the close-ended scheme is virtually dead and only a very few schemes of this nature floated during the last few months. These funds are fixed in size as regards the crops of the fund and the number of shares. In close-ended funds, no-fresh Units are created after the original offer of the scheme expires.

The Shares/Units of these funds are not redeemable at their NAV during their life as are in the case of open-ended funds. The Shares of such funds are traded in the secondary .market on stock exchanges at market prices that may be above or below their NAV.

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They are open for sale or redemption during pre-determined intervals at NAV related prices.

Based on Investment Objective

Equity Funds

Equity funds provide higher returns and at the same time, it is riskier while compared to any other fund. For long-term investment purposes, an investor is advised to invest in equity. There are different types of equity funds under different levels of risk as follows:

- Aggressive Growth Funds: The maximization of capital appreciation is the mantra for fund managers. So they invest in highly grown-up companies’ equities and less in speculative investments. Investment in speculative nature of equities may lead to higher risk.

- Growth Funds: Here, the objective is to achieve an increase in value of investment through capital appreciation and not in the regular income. Fund manager selects the companies which are expected to earn above average in future for the investment of growth funds.

- Equity Income or Dividend Yield Funds: These are for investors who are more concerned about regular returns from investments. Fund manager invests in those companies which declare high rate of dividends. Capital appreciation and risk level are less while compared to other equity funds.

- Diversified Equity Funds: Fund manger invests this type of funds in the equities of all the companies and industries without any specified industry or sector. Due to this diversification of investment, the market risk is also diversified. Example Equity Linked Savings Schemes (ELSS). (ELSS investors can claim deduction from taxable income (up to Rs 1 lakh) at the time of filing the income tax return).

- Equity Index Funds: It is based on the performance of a specific stock market index. Equity index funds are two types namely broad indices (like S&P CNX Nifty, Sensex) and narrow indices (like BSEBANKEX or CNX Bank Index etc). Investments in Narrow indices index funds are less diversifiable; therefore it is more risky than that of broad indices index funds.

- Value Funds: Fund manager invests in shares of companies which have strong financial performance but whose price-earnings ratio is low. Price-earnings ratio is the relationship between the Market Price per share and Earnings per share. These companies book value of the shares is higher than the market price.

The market price of these shares may rise in future. With this assumption the fund manager invests huge fund for long term time horizon. The cyclical industries like cement, steel, sugar etc., are the examples of value stocks. - Specialty Funds: Specialty funds are concentrated on particular industry or companies. Concentration is based on certain criteria for investments and those criteria must match with their portfolio. It is much riskier than other funds.

- Sector Funds: The portfolio of sector funds comprises of only those companies that meet their criteria.

- Foreign Securities Funds: Fund manager invests in securities of one or more foreign companies. This fund gets the advantage of international diversification, but it has to face the foreign exchange rate risk and country risk.

- Mid-Cap or Small-Cap Funds: The Mutual Fund invests in securities of those companies whose market capitalization is lower. The market capitalization of Mid-Cap companies is between ₹500 crore and ₹2500.

In case of Small-Cap companies’ market capitalization is lower than ₹500 crore. The market capitalization is the market price of the share multiplied by the number of outstanding shares of the company. The volatility of this type of companies’ securities is very high but the liquidity is very low. Due to this high volatility and low liquidity the risk of this kind of companies’ securities will be very high. - Option Income Funds: Option income funds are those funds invested in high yielding companies. The options are used for hedging activity i.e., to reduce the risk or volatility. The risk can be controlled by way of proper utilization of options. It generates stable income for investors.

- Sector Funds: The portfolio of sector funds comprises of only those companies that meet their criteria.

Money Market / Liquid Funds

Money market instruments are short-term interest bearing debt securities i.e., Treasury bills issued by Governments, (30 days, 60 days, 90 days, etc., but maturing within one year), certificate of deposits issued by banks, commercial papers issued by companies, etc.,

These securities are having high liquidity and safety. The investments in these funds are called money market/liquid funds. The risk of these funds is due to interest rate fluctuation.

Hybrid Funds

Hybrid funds comprise the portfolio of equities, debts and money market securities. The debt and equity are equal in proportion for the investment.

The types of hybrid funds in India are as follows:

- Balanced Funds: The equal proportion of debt, equity, preference and convertible securities is the portfolio of balanced funds. It gives regular income and moderates capital appreciation to investors. The risk of capital is at the minimum level. This fund is suitable for traditional investors of those who prefer long term investment.

- Growth and Income Funds: The combination of the features of growth funds and income funds is referred as Growth-and Income Funds. The capital appreciation as well as declaration of high dividend companies’ securities is comprised in the portfolio of this fund.

- Asset Allocation Funds: There are two types of investment avenues namely financial assets (equity, debt, money market instruments) and non-financial assets (real estate, gold, commodities). The fund manager may adopt the strategy of variable asset allocation. It allows change over from one asset to another at any time depending upon the market trends.

Debt / Income Funds

The investment of debt or income funds is purely only on the debt instruments issued by private companies, banks, financial institutions, governments and other entities. These funds are suitable to those investors who expect regular income and low risk.

Debt instruments are graded by credit rating agencies. The grading indicates the risk of the debt securities.

There are different types of debt funds based on investment objectives, which are as follows:-

- Diversified Debt Funds: The portfolio of the fund comprises the debt securities of all companies belonging to all industries. The result of diversified investments in all sectors is risk reduction.

- Focused Debt Funds: Debt funds that invest in debt securities issued by entities belonging to a particular sector or companies of the market are known as focused debt funds.

- High Yield Debt Funds: Generally, all debt funds have default risk. By and large, investors would like to invest in “high investment grade” securities which protect the risk of default. High yield debt funds invested in “below investment grade” securities provides high returns but the existence of default risk is higher due to more volatility.

- Assured Return Funds: The investors of this fund will get assured returns with a low-risk investment opportunity. But there may be a shortfall in returns which is borne by Asset Management Company or sponsor. The security of investments depends upon the net worth of the guarantor, whose name is specified in the offer document.

To safeguard the interest of investors, the sponsors must have adequate net worth to guarantee returns as per the norms of SEBI to offer assured return schemes.

Unit trust of India had offered ‘Monthly Income Plans’ under the scheme of assured return schemes. But the UTI had failed to fulfill its promises due to heavy shortfall in returns. The UTI’s payment obligations were taken over by the Government. Now-a-days no assured return schemes are offered in India. - Fixed Term Plan Series: The funds attracts the short-term investors and invests in short term debt securities. It is a closed-end scheme that offers a series of plans and issues units to investors at regular intervals. But these plans are not listed on the stock exchanges.

Gilt Funds

The portfolio of Gilt fund is only the government securities of medium and long-term matured bonds. It provides much safety to the investors with no credit risk. But it is exposed to interest rate risk.

- Commodity Funds: The focus of investment of this fund is on different commodities, such as metals (like gold, silver, copper etc.,), food grains, oils, etc., or options and futures, contracts of commodities, commodity producing companies etc.

The concentration of investment may be made on a specialized commodity or on a diversified commodity fund. Specialized commodity fund bears more risk than that of diversified commodity fund. - Real Estate Funds: Real estate investment provides higher capital appreciation and generates regular and higher income to the investors. Real estate investment includes not only in direct investment in real estate but also investments in securities of housing finance companies or lending to real estate developers.

- Exchange Traded Funds (ETF): Exchange Traded Funds are traded on stock exchanges like a single stock at index linked prices and it follows stock market indices. Investors of this fund get benefits of both closed-end fund and open-end mutual fund. It is very popular in London and New York stock exchanges. In India, it is introduced recently. This fund is more diversified and flexible of holding like a single share.

- Fund of Funds: It means funds of a mutual fund invested in units of mutual fund schemes offered by other Asset Management Companies. No investments are made on financial (shares, bonds) or physical assets of the Fund of Funds.

The investors of this fund get benefit of diversifying into different mutual fund schemes with a small amount of investment. And also, it facilitates diversification of risks.

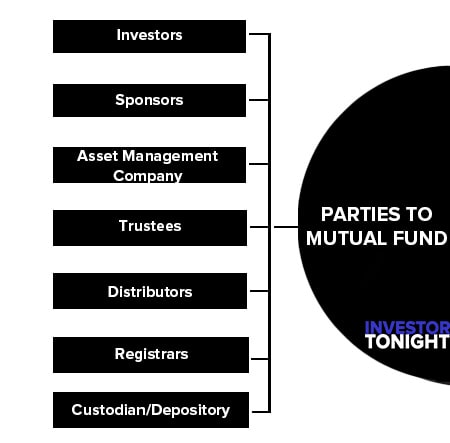

Parties to Mutual Fund

The following are the parties to mutual funds:

- Investors

- Sponsors

- Asset Management Company (AMC)

- Trustees

- Distributors

- Registrars

- Custodian/Depository

Investors

Every investor, given his/her financial position and personal disposition, has a certain inclination to take risk. The hypothesis is that by taking an incremental risk, it would be possible for the investor to earn an incremental return.

A mutual fund is a solution for investors who lack the time, the inclination or the skills to actively manage their investment risk in individual securities. They delegate this role to the mutual fund, while retaining the right and the obligation to monitor their investments in the scheme

In the absence of a mutual fund option, the money of such “passive” investors would lie either in bank deposits or other ‘safe’ investment options, thus depriving them of the possibility of earning a better return. Investing through a mutual fund would make economic sense for an investor if his/her investment, over medium to long term, fetches a return that is higher than what would otherwise have earned by investing directly.

Sponsors

The sponsor is the company, which sets up the Mutual Fund as per the provisions laid down by the Securities and Exchange Board of India (SEBI). SEBI mainly fixes the criteria of sponsors based on sufficient experience, net worth, and past track record.

Asset Management Company (AMC)

The AMC manages the funds of the various schemes and employs a large number of professionals for investment, research and agent servicing. The AMC also comes out with new schemes periodically. It plays a key role in the running of mutual fund and operates under the supervision and guidance of the trustees. An AMC’s income comes from the management fees, it charges for the schemes it manages. The management fees, is calculated as a percentage of net assets managed.

An AMC has to employ people and bear all the establishment costs that are related to its activity, such as for the premises, furniture, computers and other assets, etc. So long as the income through management fees covers its expenses, an AMC is economically viable. SEBI has issued the following guidelines for the formation of AMCs:

- An AMC should be headed by an independent non-interested and nonexecutive chairman.

- The managing director and other executive staff should be full-time employees of AMC.

- Fifty per cent of the board of trustees of AMC should be outside directors who are not in any way connected with the bank.

- The board of directors shall not be entitled to any remuneration other than the sitting fees.

- The AMCs will not be permitted to conduct other activities such as merchant banking or issue management.

Trustees

Trustees are an important link in the working of any mutual fund. They are responsible for ensuring that investors’ interests in a scheme are taken care of properly. They do this by constant monitoring of the operations of the various schemes. In return for their services, they are paid trustee fees, which are normally charged to the scheme.

Distributors

Distributors earn a commission for bringing investors into the schemes of a mutual fund. This commission is an expense for the scheme. Depending on the financial and physical resources at their disposal, the distributors could be:

- Tier 1 distributors who have their own or franchised network reaching out to investors all across the country; or

- Tier 2 distributors who are generally regional players with some reach within their region; or

- Tier 3 distributors who are small and marginal players with limited reach. The distributors earn a commission from the AMC.

Registrars

An investor’s holding in mutual fund schemes is typically tracked by the schemes’ Registrar and Transfer Agent (R & T). Some AMCs prefer to handle this role on their own instead of appointing R & T. The Registrar or the AMC as the case may be maintains an account of the investors’ investments and disinvestments from the schemes. Requests to invest more money into a scheme or to redeem money against existing investments in a scheme are processed by the R & T.

Custodian/Depository

The custodian maintains custody of the securities in which the scheme invests. This ensures an ongoing independent record of the investments of the scheme. The custodian also follows up on various corporate actions, such as rights, bonuses and dividends declared by investee companies.

At present, when the securities are being dematerialized, the role of the depository for such independent records of investments is growing. No custodian in which the sponsor or its associates hold 50 percent or more of the voting rights of the share capital of the custodian or where 50 percent or more of the directors of the custodian represent the interest of the sponsor or its associates shall act as custodian for a mutual fund constituted by the same sponsor or any of its associates or subsidiary company.

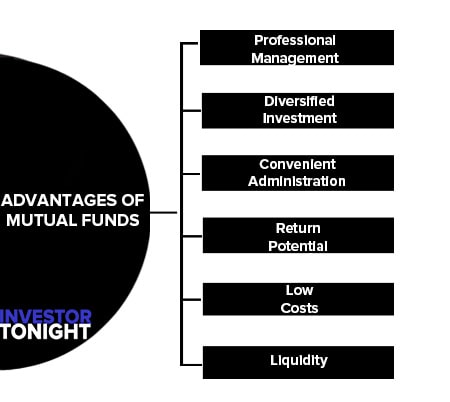

Advantages of Mutual Funds

Following are some of the advantages of mutual funds:

- Professional Management

- Diversified Investment

- Convenient Administration

- Return Potential

- Low Costs

- Liquidity

Professional Management

The investor avails of the services of experienced and skilled professionals who are backed by a dedicated investment research team which analyses the performance and prospects of companies and selects suitable investments to achieve the objectives of the scheme.

Diversified Investment

Mutual Funds invest in a number of companies across a broad crosssection of industries and sectors. This diversification reduces the risk because seldom do all stocks decline at the same time and in the same proportion. This diversification is achieved through a Mutual Fund.

Convenient Administration

Investing in a Mutual Fund reduces paperwork and helps to avoid many problems such as bad deliveries, delayed payments and follow up with brokers and companies. Mutual Funds save time and makes investing easy and convenient.

Return Potential

Over medium to long term, Mutual Funds have the potential to provide a higher return as they invest in a diversified basket of selected securities.

Low Costs

Mutual Funds are a relatively less expensive way to invest compared to directly investing in the capital markets because of the benefits of scale in brokerage, custodial and other fees which translate into lower costs for investors.

Liquidity

In open-end schemes, an investor can get his money back promptly at net asset value. With closed-ended schemes, an investor can sell his units on a stock exchange at the prevailing market price or avail of the facility of direct repurchase at NAV related prices which some close ended and interval schemes offer periodically.

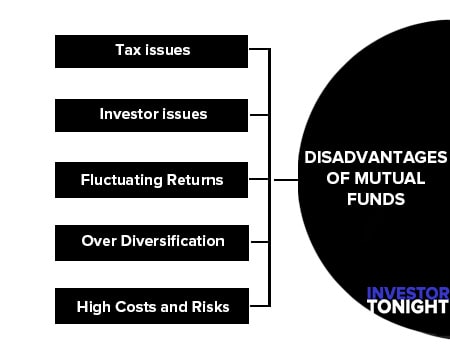

Disadvantages of Mutual Funds

Following are some of the disadvantages of mutual funds:

Tax issues

Although the returns on investment are quite high, a mutual fund cannot guarantee lower tax bills. The tax amounts are usually high, especially in the case of short-term gains.

Investor issues

A mutual fund requires a deep and long-term analysis of the amount of investment and its potential investment areas. If the company fund manager changes regularly, it may adversely affect the returns on investment.

Fluctuating Returns

Mutual funds are like many other investments where there is always the possibility that the value of the mutual fund will depreciate, unlike fixed income products, such as bonds and treasury bills, mutual funds experience price fluctuations along with the stocks that make up the fund.

Over Diversification

Although diversification is one of the keys to successful investing, many mutual fund investors tend to over diversify. The idea of diversification is to reduce the risks associated with holding a single security; over diversification occurs when investors acquire many funds that are highly related and, as a result, reduce the benefits of diversification.

High Costs and Risks

Mutual funds provide investors with professional management, but it comes at a cost. Funds will typically have a range of different fees that reduce the overall payout. In mutual funds, the fees are classified into two categories: shareholder fees and annual operating fees.

The shareholder fees, in the forms of loads and redemption fees, are paid directly by shareholders purchasing or selling the funds. The annual fund operating fees are charged as an annual percentage – usually ranging from 1-3%. These fees are assessed to mutual fund investors regardless of the performance of the fund. Mutual funds are subjected to market risks or assets risks. If the investment is not sufficiently diversified, it may involve huge losses.

SEBI Guideline of Mutual Fund : SEBI Regulation Act 1996

In India mutual fund play the role as investment with trust, some of the formalities laid down by the SEBI to be establishment for setting up a mutual fund. As the part of trustee sponsor the mutual fund, under the Indian Trust Act, 1882, under the trustee company are represented by a board of directors.

Board of Directors is appoints the AMC and custodians. The board of trustees made relevant agreement with AMC and custodian. The launch of each scheme involves inviting the public to invest in it, through an offer documents. Depending on the particular objective of scheme, it may open for further sale and repurchase of units, again in accordance with the particular of the scheme, the scheme may be wound up after the particular time period.

- The sponsor has to register the mutual fund with SEBI.

- To be eligible to be a sponsor, the body corporate should have a soundtrack record and a general reputation of fairness and integrity in all his business transactions.

Means of Sound Track Records

The body corporate being in the financial services business for at least five years Having a positive net worth in the five years immediately preceding the application of registration.

Net worth in the immediately preceding year more than its contribution to the capital of the AMC.

Earning a profit in the three out of the five preceding years, including the fifth year. - The sponsor should hold at least 40% of the net worth of the AMC.

- A party which is not eligible to be a sponsor shall not hold 40% or more of the net worth of the AMC.

- The sponsor has to appoint the trustees, the AMC and the custodian.

- The trust deed and the appointment of the trustees have to be approved by SEBI.

- An AMC or its officers or employees cannot be appointed as trustees of the mutual fund

- At least two thirds of the business should be independent of the sponsor.

- Only an independent trustee can be appointed as a trustee of more than one mutual fund, such appointment can be made only with the prior approval of the fund of which the person is already acting as a trustees.

Launching of a Schemes

Before its launch, a scheme has to be approved by the trustees and a copy of its offer documents filed with the SEBI.

- Every application form for units of a scheme is to be accompanies by a memorandum containing key information about the scheme.

- The offer document needs to contain adequate information to enable the investors to make informed investments decisions.

- All advertisements for a scheme have to be submitted to SEBI within seven days from the issue date.

- The advertisements for a scheme have to disclose its investment objective.

- The offer documents and advertisements should not contain any misleading information or any incorrect statement or opinion.

- The initial offering period for any mutual fund schemes should not exceed 45 days, the only exception being the equity linked saving schemes.

- No advertisements can contain information whose accuracy is dependent on assumption.

- An advertisement cannot carry a comparison between two schemes unless the schemes are comparable and all the relevant information about the schemes is given.

- All advertisements need to carry the name of the sponsor, the trustees, the AMC of the fund.

- All advertisements need to disclose the risk factors.

- All advertisements shall clarify that investment in mutual funds is subject to market risk and the achievement of the fund’s objectives cannot be assured.

- When a scheme is open for subscription, no advertisement can be issued stating that the scheme has been subscribed or over subscription.

Mutual Fund Myths

There are few myths and misconceptions associated with investing in mutual fund schemes. Some of these notions have faded over time, as investor awareness has increased but some continue to hold strong. It is imperative to dispel these myths as investments should not be made under wrong impressions.

It can throw the best laid out financial plan out of control, and the situation can be avoided with a little bit of caution.

The most common myth that is prevalent among mutual fund investors is that of associating a scheme with a lower NAV being a better buy compared to a scheme with a higher NAV. This stems from the mind set of equating mutual fund units with equity shares of a company. NAV of a scheme is irrelevant and irrespective of whether we are investing into a fund having a low NAV or a fund with a higher NAV, the amount of investment remains the same.

Let’s look at a hypothetical investment into two schemes A and B. Scheme A has a NAV of Rs 10 whereas scheme B has a NAV of Rs 200. We made equal amount of investment of Rs. 1 lakh each in both the schemes. Scheme A would come across as a cheaper buy because we got 10,000 units as against 500 units in scheme B. Now, let us assume that both the scheme returns 10 % in a month. The NAV for scheme A is Rs 11 and Scheme B has a NAV of Rs 220. The value of your investment in both the case is Rs 1,10,000.

Therefore, we see that the NAV of a scheme is irrelevant, as far as generating returns is concerned. The only difference being in case of the former, the investor gets more units and in the latter, he gets lesser units. For two schemes with identical portfolio and other things remaining constant, the difference in NAV will hardly matter and both the schemes will grow at the same rate.

Regular Dividends Means Good Performance

Another popular myth which emerges due to the linkages we make between the concepts of stock markets and mutual funds is the dividend payout mechanism. When a company pays dividends, in effect it is transferring acerta in a portion of its surplus to its shareholders. Therefore a generous dividend payout policy could be considered favorable in case of a company.

However, in case of mutual funds, dividends are declared out of the distributable surplus which is included in the calculation of net asset value. In effect it is paying back a certain portion of net assets from our own investments. Therefore, dividends from mutual fund units don’t make us any richer, as there are no additional gains to be made. The NAV of the scheme falls to the extent of the dividend payout, when a scheme pays dividend.

Thus, a scheme with a high dividend payout record does not necessarily mean that it is performing well. Dividend option may prove important to plan cash flows, especially in the case of tax savings schemes which have a lock-in period and also for tax incidence.

Demat Account is Required for MF investments

Except in case of schemes which are listed on the stock exchange and are available on their platforms, demat account is not required to own units in a mutual fund scheme.

Past Performers are the Best Funds to Buy

Despite the disclaimers, mutual fund investors tend to invest in the top performing scheme of the last year, hoping that past performance will ensure that the scheme continues to stay at the top. Therefore, instead of chasing the top performer in the short term, it is advisable to invest in a scheme which features in the top quartile consistently over a longer period of time. In addition to past performance, the investors should also consider other factors viz. professional management, service standards etc.

Fees and Expenses

As is the case with any other business, running a mutual fund business also involves costs. The various costs incurred by a mutual fund could be associated with transactions made by investors, operating costs, marketing and distribution expenses etc. Expenses borne by the mutual fund investor can be broadly classified into two categories:

- The load which may be charged to the investor at the time of redemption

- The recurring expenses which are charged to the fund.

Loads or Sales Charges: Loads are charges which investors incur when they redeem units in a mutual fund scheme. A load charged at the time of redemption is known as ‘Exit Load or Back End Load’. Asset management companies charge these loads to defray the selling and distribution expenses including commission paid to the agents/distributors.

Since August 1, 2009 entry load has been banned and therefore purchase/subscription of mutual funds happen at a price which is equal to the NAV. However, an investor is required to pay an exit load (if any) if he chooses to redeem units. This happens at a price linked to the NAV. This re-purchase price price may differ from NAV to the extent of exit load charged, if any.

Further, expenses related to New Fund Offer (NFO) are borne by the AMC/Trustee /Sponsor.

Recurring Expenses

These are costs incurred for day to day operation of a scheme. These expenses inter alia include investment management and advisory fees, trustee fees, registrar’s fees, custodian’s fees, Audit fees, marketing and selling expenses including agents’ commission etc. Expenses exceeding the specified limit are to borne by the AMC.

Brokerage and Transaction Cost

In addition to limits specified in regulation 52 (6) of the Regulations, brokerage and transaction costs incurred for the purpose of execution of trade not exceeding 0.12% of value of trade in case of cash market transaction and 0.05% of value of trade in case of derivative transactions (inclusive of service tax) will be capitalised.

Any payment towards brokerage and transaction cost for execution of trade, over and above the said limit of 0.12% for cash market transactions and 0.05% for derivatives transactions may be charged to the scheme within the maximum limit of TER as prescribed under regulation 52 of the Regulations.

Establish Your Financial Goals for Mutual Fund

Before you enter the world of mutual funds, it’s crucial that you meet with a financial advisor to discuss your financial goals. Your advisor uses these goals to help you create a plan for building wealth. Periodic meetings with your advisor — especially when your financial goals or circumstances change — help ensure that your investment strategy meets your needs.

As you prepare to meet with your financial advisor, ask yourself the following questions:

What are my financial goals, and when will I need the money?

Perhaps you’re saving for a house, your child’s college education or retirement. These are all considerations that affect how much risk you can afford to take and what funds you buy

How much can I afford to invest?

You may not have much to invest right now, but you may be able to invest as little as 500-1000 per month in mutual funds. Whatever your situation, a financial advisor can help you create a plan to start saving to achieve your goals.

Which is more important to me: the stability of the investment (potentially less risk and lower returns) or higher returns on my investment (potentially higher risk)?

All mutual funds carry a certain amount of risk, including the possible loss of your investment. Generally, the longer it is until you need your money, the more risk you can afford to take. Your financial advisor can help you decide how much — or how little — risk is appropriate for your situation.

Once you have answered these questions, you’ll have a good outline of where you want to be financial. Now you and your financial advisor can explore which mutual funds may help you get there.