Foreign Exchange Market in India

The foreign market in India has three segments.

- The first segment consists of transactions between RBI and the authorized dealer (AD).

- The second segment is the interbank market in which the banks deal among themselves.

- The third segment is the retail segment in which the ADs deal with the corporate clients and other retail customers.

Table of Contents

First Tier of Foreign Exchange Market

Under the first tier, transactions take place between the Reserve Bank of India (RBI) and the authorized dealers (ADs). The responsibility and authority of foreign exchange administration lies with the RBI.

This authority has been provided to the RBI under the Foreign Exchange Regulation Act. RBI is considered to be the apex body and for convenience has delegated the responsibility of foreign exchange transactions to ADs which are the scheduled commercial banks.

A Foreign Exchange Dealers Association of India has been formed which makes rules and regulations regarding how a business will be conducted and also coordinates with the RBI in the administrative functions related to foreign exchange control. It basically acts as a clearing house.

In the first tier of the foreign exchange market, the RBI buys and sells foreign currency from and to ADs as per the prevalent exchange control regulations from time to time. Before the Liberalized Exchange Rate Management System was introduced, ADs sold foreign currency at rates administered by the RBI. RBI sold pound sterling, US dollars, spot as well as forward to the ADs in order to cover ADs primary market requirement.

However, with the introduction of a unified exchange rate system, the RBI now intervenes in the market to stabilize the value of the rupee.

Second Tier of Foreign Exchange Market

The interbank market forms the second tier of the foreign exchange market. In the second tier of foreign exchange market, transactions take place between ADs.

Although, ADs mainly conduct their business within their own country, but through interbank markets are able to conduct business with banks in different countries in order to cover their position. Although business transactions can be done independently, many prefer to conduct their business through recognized brokers.

One important aspect regarding interbank market transactions is that the brokers are not permitted to execute any deal on behalf of their own account or for jobbing purposes. Interbank transactions taking place within the country are both spot as well as forward. There may be swap transactions. During these transactions, any permitted currency may be used.

Forward trading with overseas banks is allowed if it covers genuine transactions or for the purpose of squaring currency position. It needs to be ensured that the forward trading does not exceed more than six months. In case an import is made on deferred payment and the period exceeds six months, then permission has to be obtained from RBI.

Though forward contracts are permitted to be canceled in India, it needs to be referred to RBI. Prior to 1994-95, the banks were responsible to cover these forward transactions with RBI, but now RBI does not provide this cover. With RBI’s permission, the banks trade with complete freedom in the forward market. In order to cancel a forward contract, it needs to enter into a reverse transaction as per the current going rate.

Similarly, if the value of the US dollar increases on the time of cancellation, then the customer will make profits in this transaction. Now canceled forward contracts that fall within the time period of one year, maybe re-booked as RBI now permits ADs to do so

Third Tier of Foreign Exchange Market

The primary market where ADs make transactions in foreign currency with customers forms the third tier of the foreign exchange market.

The third tier of the foreign exchange market primarily exists as the outcome of legal regulations which state that if Indian residents need to make foreign exchange transactions then they must take place via ADs.

Primary market is inclusive of the following:

- Tourist exchange currency

- Exporters exchange currency

- Importers exchange currency

The branches of ADs are divided into three categories that are as follows:

- Category A: In this category, the branches maintain independent foreign currency accounts with oversea branches in their own names.

- Category B: The branches in this category do not maintain independent foreign currency accounts but have powers to operate the accounts maintained abroad by their head offices or the category A branches.

- Category C: The branches that are not allocated in A or B category but are still in forex business are included in this category.

In the retail segment, money changers also operate. These are licensed dealers in the currency market to cater to the needs of retail customers. In the interbank market, the quotes appear in swap points. There are currency brokers who match the buyers and sellers and work on a commission basis.

Derivative markets

Derivative markets are for those assets which are synthetic financial products derived from real assets or stock or commodities. After the floating exchange rate system replaced the fixed exchange rate system, there was high volatility in some currencies due to speculation. The regulatory bodies were forced to find new ways to reduce the risk attached to the Forex business.

For managing risks on account of volatility in the exchange rates and interest rates, new products were designed and were called derivatives. They derive their value from other products. These are used for risk reduction from the high volatility of financial markets. The major problem of these derivative markets is over speculation which has to be controlled by a right degree of regulation.

Derivative market includes the following instruments:

- Forward Rate Agreements (FRAs): It is a contact for delivery of foreign currency at a specified future date at a fixed exchange system.

- Swaps: It is a deal in which a bank buys a specified foreign currency and sells the same at different maturity dates.

- Options: The contracts with a right to buy or sell a stated currency without any obligation, at a fixed rate on a future date.

Classification of Derivatives

- DERIVATIVES

- FINANCIALS

- BASIC

- Forwards

- Futures

- Options

- Warrants & Convertibles

- COMPLEX

- Swaps

- Exotics

- BASIC

- FINANCIALS

- COMMODITIES

History of Derivative Markets

The first evidence of future market can be traced to 12th century in England and France. Forward trading started in 17th century in Japan. The forward markets dealt with rice were known as Cho-at-mai meaning rice trade on book.

In 1730, this market was officially recognized and thus, became the first futures market and was registered as an organized exchange. In 1898, butter and eggs dealers of Chicago Produce Exchange came together to form Chicago Mercantile Exchange for futures trading.

This provided an organized market where many commodities were traded. The International Monetary Market was formed as a division of the Chicago Mercantile Exchange in 1972 which was followed by the London International Financial Futures Exchange in 1982.

The derivatives are used to provide the following services:

- The main service provided by the derivatives is to control, avoid, shift and manage different types of risks through different techniques like hedging and arbitraging.

- Derivatives act as barometers of the future trends in prices that will help in establishing new prices both on the spot and futures markets.

- Derivative trading is based on margin trading and the players in the market do not have to make the full payment at the time of trade. This encourages the presence of many players in the market thus making it highly competitive market.

- Derivatives help the players of the market to develop strategies to make proper asset allocation and thus increase their yield.

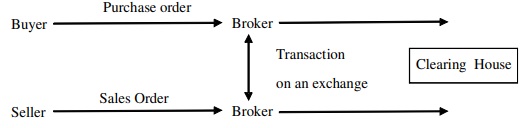

Foreign Currency Futures

Foreign currency futures are the contacts specifying a volume of a particular currency to be exchanged on specific settlement data that can be used to hedge the foreign exchange risk.

In 1919, the Chicago Mercantile Exchange (CME) was established as a commodity future exchange for farmers and users of agricultural goods. In 1972, CME established the International Money Market (IMM) division that allows trading of futures of short-term securities, gold and foreign currencies.

Comparison of Forward Contracts and Currency Future Contracts

- Both Forward contracts and currency futures allow the buyer to lock in the price to be paid for a given currency at a future point in time.

- Currency futures are traded face-to-face but forward contracts are negotiated over phone.

- Currency future deals are standardized and can be traded on floor where as the contacts are customized therefore hey cannot be traded on floor of the exchange.

In the currency future market, different currencies are sold and purchased at a specified future date at a predetermined price and of a specified quantity on a particular recognized exchange.

Features of currency futures:

- It is traded on organized exchanges.

- They are standardized.

- After a contract is agreed between two parties, the agreement is cleared by a clearing house.

Trading Process

In the most futures markets, actual physical delivery of the underlying assets is very rare. Most often buyers and sellers offset their original position p