What is Bank?

Bank is a lawful organization which accepts deposits that can be withdrawn on demand. It also tends money to individuals and business houses that need it.

Table of Contents

- 1 What is Bank?

- 2 Bank Definition

- 3 Types of Banks

- 4 Types of Banking

- 5 Importance of Banks

- 6 Role of Banks in Economic Development

- 6.1 Mobilizing Saving for Capital Formation

- 6.2 Financing Industry

- 6.3 Generate Employment Opportunities

- 6.4 Smoothing of trade and commerce functions

- 6.5 Financing Agriculture

- 6.6 Application of Monetary Policy

- 6.7 Financing Small Businesses

- 6.8 Promotion of Saving Habits

- 6.9 Support the Government Spending

- 6.10 Arbiters of Risk

Bank Definition

Banking Company is one which transacts the business of banking which means the accepting for the purpose of lending or investment of deposits money from the public repayable on demand or otherwise and withdrawable by cheque, draft, order or otherwise. – Indian Banking Companies Act

The oxford dictionary defines a bank as “an establishment for custody of money received from or on behalf of its customers. It’s essential duty is to pay their drafts on it. It’s profits arises from the use of the money left employed by them“.

The Webster’s Dictionary, “an institution which trades in money, establishment for the deposit, custody, and issue of money, as also for making loans and discounts and facilitating the transmission of remittances from one place to another”.

According to Prof. Kinley, “A bank is an establishment which makes to individuals such advances of money as may be required and safely made, and to which individuals entrust money when it required by them for use“.

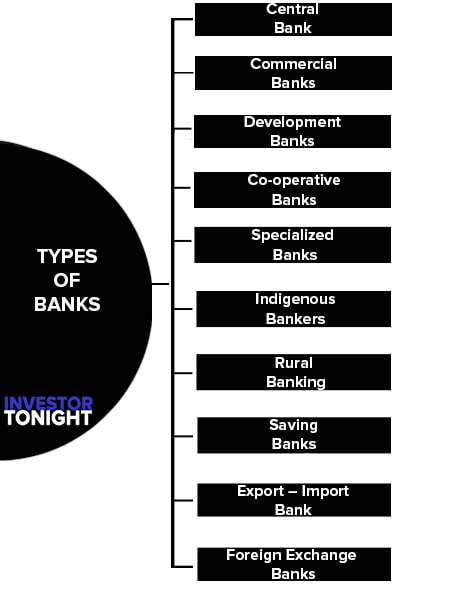

Types of Banks

There are various types of banks which operate in our country to meet the financial requirements of different categories of people engaged in agriculture, business, profession etc. on the basis of functions, the banking institution may be divided into the following types:

- Central Bank

- Commercial Banks

- Development Banks

- Co-operative Banks

- Specialized Banks

- Indigenous Bankers

- Rural Banking

- Saving Banks

- Export – Import Bank

- Foreign Exchange Banks

Central Bank

A central bank functions as the apex controlling institution in the banking and financial system of the country. It functions as the controller of credit, banker’s bank and also enjoys the monopoly of issuing currency on behalf of the government.

A central bank is usually control and quite often owned, by the government of a country. The Reserve Bank of India (RBI) is such a bank within India.

Commercial Banks

It operates for profit. It accepts deposits from the general public and extends loans to households, the firms and the government. The essential characteristics of commercial banking are as follows:

- Acceptance of deposits from public

- For the purpose of lending or investment

- Repayable on demand or lending or investment

- Withdrawal by means of an instrument, whether a cheque or otherwise.

Another distinguishing feature of a commercial bank is that a large part of their deposits are demand deposits withdrawable and transferable by cheque.

Development Banks

It is considered as a hybrid institution which combines in itself the functions of a finance corporation and a development corporation. They also act as a catalytic agent in promoting balanced and viable development by assuming the promotional role of discovering project ideas, undertaking feasibility studies and also provide technical, financial and managerial assistance for the implementation of project.

In India ‘Industrial Development Bank on India’ (IDBI) is a unique example of a development bank. It has been designated as the principal institution of the country for coordinating the working of the institutions engaged in financing, promoting or development of the industry.

Co-operative Banks

The main business of cooperative banks is to provide finance to agriculture. They aim at developing a system of credit. Agriculture finance is a special field.

The cooperative banks play a useful role in providing cheap exit facilities to the farmers. In India there are three wings of cooperative credit system namely:

- Short term

- Medium-term

- Long term credit.

The former has a three-tier structure consisting of state cooperative banks at the state level. At the intermediate level (district level) these are central co-operative banks, which are generally established for each district. At the base of the pyramid, there are primary agricultural societies at the village level.

The long-term exit is provided by the central land development Bank established at the state level. Initially, these banks used to advance loans on a mortgage of land for the purpose of securing the repayment of loans.

Specialized Banks

These banks are established and controlled under the special act of parliament. These banks have got the special status. One of the major bank is ‘National Bank for Agricultural and Rural development’ (NABARD) established in 1982, as an apex institution in the field of agricultural and other economic activities in rural areas.

In 1990 a special bank named small industries development Bank of India (SIDBI) was established. It was the subsidiary of Industrial development Bank of India. This bank was established for providing loan facilities, discounting and rediscounting of bills, direct assistance and leasing facility.

Indigenous Bankers

That unorganised unit which provides productive, unproductive, long term, medium-term and short term loan at the higher interest rate are known as indigenous bankers. These banks can be found everywhere in cities, towns, mandis and villages.

Rural Banking

A set of financial institution engaged in financing of rural sector is termed as ‘Rural Banking’. The polices of financing of these banks have been designed in such a way so that these institution can play catalyst role in the process of rural development.

Saving Banks

These banks perform the useful services of collecting small savings commercial banks also run “saving bank” to mobilise the savings of men of small means. Different countries have different types of savings bank viz. Mutual savings bank, Post office saving, commercial saving banks etc.

Export – Import Bank

These banks have been established for the purpose of financing foreign trade. They concentrate their working on medium and long-term financing. The Export-Import Bank of India (EXIM Bank) was established on January 1, 1982 as a statutory corporation wholly owned by the central government.

Foreign Exchange Banks

These banks finance mostly to the foreign trade of a country. Their main function is to discount, accept and collect foreign bulls of exchange. They also buy and self foreign currencies and help businessmen to convert their money into any foreign currency they need. Over a dozen foreign exchange banks branches are working in India have their head offices in foreign countries.

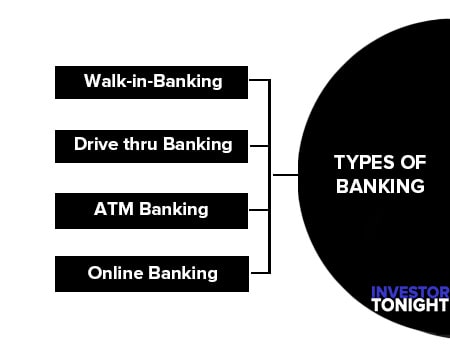

Types of Banking

Banking is described as the business carried on by an individual at a bank. Today, several forms of banking exist, giving consumers a choice in the way they manage their money most people do a combination of at least two banking types.

However, the type of banking a consumer uses normally based on convenience. These are different types of banking through which consumer can attach to it:

Walk-in-Banking

It is still a popular type of banking. As, in the past, it still involves bank tellers and specialized bank officers. Consumers must walk into a bank to use this service normally, in order to withdraw money or deposit it, a person must fill out a slip of paper with the account and specific monetary amount and show a form of identification to a bank letter.

The advantage of walk-in Banking is the face-to-face connection between the banker and a letter. Also unlike drive-thru and ATM banking, a person can apply for a loan and invest money during a walk-in.

Drive thru Banking

It is probably the least popular form of banking today but is still used enough by consumers to create a need for it. It allows consumers to stay in their while and drive up to a machine equipped with a container, chute and intercom. This machine is connected to a bank and is run by one or two bank letters.

A person can withdraw or deposit money at a drive-thru. He must fill out a slip with his account and the specific monetary amount and put it in the container. The container travels through the chute to the bank letter, who will complete the banker’s request. This is where the intercom comes into play. The bank teller and banker use it to communicate and discuss the specific banking request.

ATM Banking

It is very popular because it gives a person 24-hour access to his bank account. Walk-in and drive-thru banking does not offer this perk. In order to use an ATM, a person must have an ATM card with a personal identification number (PIN) and access to an ATM machine.

Any ATM machine can be used, but charges apply if the ATM machine is not affiliated with the bank listed on the ATM card. By sliding an ATM card into an ATM machine, it is activated and then through touching buttons on the machine, a consumer is able to withdraw or deposit money.

Online Banking

It allows a person to get on the internet and sign into their bank. This process is achieved with the use of a PIN, different from the one used for the ATM card. By going website of a bank and entering it, a consumer can get into his account, withdraw money, deposit money, pay bills, request loans and invest money.

Online banking is growing in popularity because of its convenience. These different types of banking give a consumer the power of choice and also give them a comfortable banking system that gives them a convenient choice.

Importance of Banks

Banks play an important role in the economic growth of a country. In the modern setup, banks are not to be considered dealers in money but as the leaders of development.

The importance of bank for a country’s economy can be explained in the following ways:

- Banks by playing attractive interest rate on deposits try to promote thrift and savings in an economy. The investment of these savings in productive channel results in capital formation.

- The scattered small savings in the country can be put to optimum use by commercial banks. Banks utilize this amount by giving loans to industrial houses and the government. By providing funds to the entrepreneurs, bank help in increasing productivity of capital.

- Banks help in remitting money from one place to another. The cheque, bank draft, letter of credit, bills, hundies enable traders to transfer large sums of money from one place to another.

- By their ability to create credit, the banks have placed at the disposal of the nation a large amount of money. The bank can increase the supply of money through credit creation.

- With the growth of banking activity, employment opportunity in the country has increased to a considerable extent.

- The banks help in capital formation in the country. A high rate of saving and investment promote capital formation.

- Money deposited in the bank and other precious items are now absolutely safe. For keeping valuables, banks are providing locker facilities. Now people are free from any type of risks.

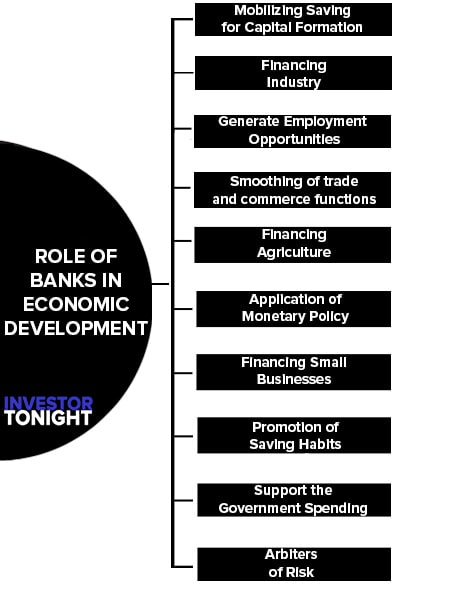

Role of Banks in Economic Development

- Mobilizing Saving for Capital Formation

- Financing Industry

- Generate Employment Opportunities

- Smoothing of trade and commerce functions

- Financing Agriculture

- Application of Monetary Policy

- Financing Small Businesses

- Promotion of Saving Habits

- Support the Government Spending

- Arbiters of Risk

Mobilizing Saving for Capital Formation

Commercial banks help in mobilizing savings through a network of branch banking. People in developing countries have low incomes but the banks encourage them to save by introducing a variety of deposit schemes to suit the needs of individual depositors.

They also mobilize idle savings of the few rich. By mobilizing savings, the banks channelize them into productive investments. Thus they help in the capital formation of a developing country.

Financing Industry

Commercial banks finance the industrial sector in a number of ways. In general, they provide short-term, medium-term, and long-term loans to the industry. In India, they provide mainly short-term loans as well medium-term loans for one to three years. But in Korea, commercial banks also advance long-term loans to industry.

Generate Employment Opportunities

Since a bank promotes industry and investment, there automatically generate employment opportunities. So, a bank enables an economy to generate employment opportunities.

Smoothing of trade and commerce functions

In this modern era trade and commerce play a vital role in any country. So, the money transaction should be user-friendly. A modern bank helps its customers to sent funds to anywhere and receive funds from anywhere of the world.

A well-developed banking system provides various attractive services like mobile banking, internet banking, debit cards, credit cards, etc. these kinds of services fast and smooth the transactions. So, the bank helps to develop trade and commerce.

Financing Agriculture

Commercial banks help the large agricultural sector in developing countries in a number of ways. They provide loans to traders in agricultural commodities. They provide finance directly to farmers for the marketing of their produce, for the modernization and mechanization of their farms, for providing irrigation facilities, for developing land, etc.

They also provide financial assistance for animal husbandry, dairy farming, sheep breeding, poultry farming, and horticulture.

Application of Monetary Policy

Monetary policy is an important policy of any government. The major aim of the monitory policy is to stabilize the financial system of the country from the dangers of inflation, deflation, crisis, etc.

Financing Small Businesses

Commercial banks also finance business lending in a variety of ways. A business owner may solicit a loan to finance the start-up costs of a small business. Once funded, the small business may begin operations and embark on a growth plan. The aggregate effect of small business activity generates a significant portion of employment around the country.

According to the U.S. Census Bureau, businesses employing between one and 19 people accounted for 4.4 million jobs in 2004. In contrast, businesses with more than 20 employees only accounted for 1.2 million in the same year.

Promotion of Saving Habits

Bank attracts depositors by introducing attractive deposit schemes and providing rewards or return in the form of interest. Banks providing different kinds of deposit schemes to its customers. It enables to create of banking habits or saving habits among people.

Support the Government Spending

Commercial banks also support the role of the federal government as an agent of economic development. Generally, commercial banks help fund government spending by purchasing bonds issued by the Department of the Treasury. Both long and short-term Treasury bonds help finance government operations, programs and support deficit spending.

Arbiters of Risk

One of the most significant roles of commercial banks in economic development is as arbiters of risk. This occurs primarily when banks make loans to businesses or individuals. For instance, when individuals apply to borrow money from a bank, the bank examines the borrower’s finances, including income, credit score and debt level, among other factors. The outcome of this analysis helps the bank gauge the likelihood of borrower default.

By weeding out risky borrowers, commercial banks lessen the risk of financial losses. As a result, loans that mature without any problems generate a larger pool of funds for the bank to lend, further supporting economic development. Modern banks are spreading its operations throughout the world.

We can see a number of big banks like HDFC bank, Baroda bank, ICICI Bank etc. It helps a country to spread banking activities in rural and semi-urban areas. With the spreading of banking operations around the country, helps to attain balanced development by promoting rural areas.

The modern bank plays a vital role in the socio-economic development of the country. A developed banking system enables the country to attain balanced development without any special consideration of rich and poor, cities and rural areas etc