What is Letter of Credit?

Letters of Credit’ (L/C) also known as ‘Documentary Credits’ is the most commonly accepted instrument of settling international trade payments. A Letter of Credit is an arrangement whereby the bank acting at the request of a customer (importer/buyer), undertakes to pay for the goods/ services, to a third party (exporter/beneficiary) by a given date, on documents being presented in compliance with the conditions laid down.

Table of Contents

Letter of Credit Definition

Further, the several definitions of L/C are given as:

- A Letter of Credit (L/C) is a document containing the guarantee of a bank to honour drafts drawn on it by an exporter, under certain conditions and up to certain amounts, provided that the beneficiary fulfils the stipulated conditions.

- A Letter of Credit (L/C), simply defined, is a written instrument issued by a bank at the request of its customer, the importer (buyer), whereby the bank promises to pay the exporter (beneficiary) for goods or services, provided that the exporter presents all documents called for, exactly as stipulated in the L/C, and meet all other terms and conditions set out in the L/C

- The International Chamber of Commerce (ICC) in the Uniform Custom and Practice for Documentary Credit (UCPDC) defines documentary credit as:

“An arrangement, however, named or described, whereby a bank (the issuing bank) acting at the request and in accordance with the instructions of a customer (the applicant to the credit) to make payment to or to the order third party (the beneficiary) or is to pay, accept or negotiate bills of exchange (drafts) drawn by the beneficiary, or authorize such payments to be made or such drafts to be paid, accepted or negotiated, by another bank, against stipulated documents and compliance with stipulated terms and conditions.”

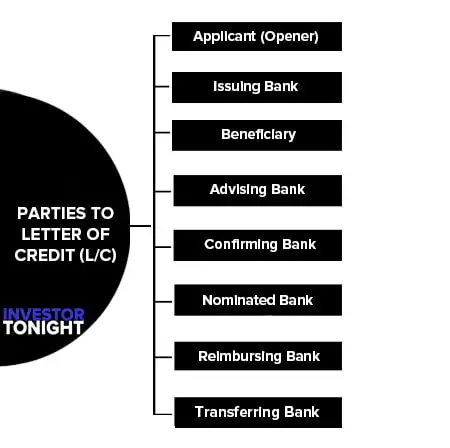

Parties to Letter of Credit (L/C)

- Applicant (Opener)

- Issuing Bank (Opening Bank)

- Beneficiary

- Advising Bank

- Confirming Bank

- Nominated Bank

- Reimbursing Bank

- Transferring Bank

Applicant (Opener)

The (applicant/buyer/customer/importer) of the goods, who has to make payment to beneficiary, L/C is opened and issued on the basis of his request and instructions.

Issuing Bank (Opening Bank)

The bank issuing the L/C is known as “issuing” bank.

Beneficiary

The beneficiary is the seller/exporter of the goods, who has to receive payment from the applicant.

Advising Bank

The “advising” bank provides advice to the beneficiary and takes the responsibility for sending the documents to the issuing bank and is normally located in the country of the beneficiary.

Confirming Bank

The “confirming” bank adds its guarantee to the credit opened by another bank, thereby undertaking the responsibility of payment/negotiation acceptance under the credit, in addition to that of the issuing bank. The confirming bank serves an important role where the exporter is not satisfied with the undertaking of only the issuing bank. It is situated in exporter’s country and if issuing bank fails, the confirming bank has to honours its commitment.

Nominated Bank

A bank in an exporter’s country which is specifically permitted by the issuing bank to receive, negotiate, etc., the documents and pays the amount to the exporter under the L/C.

Reimbursing Bank

A bank authorised to honour the reimbursement claim made by the paying, accepting or negotiating bank. It is normally the bank with which issuing bank has Nostro Account from which the payment is made to the nominated bank.

Transferring Bank

In a transferable L/C, the 1st beneficiary may request the nominated bank to transfer the L/C in favour of one or more second beneficiaries. Such a bank is called transferring Bank.

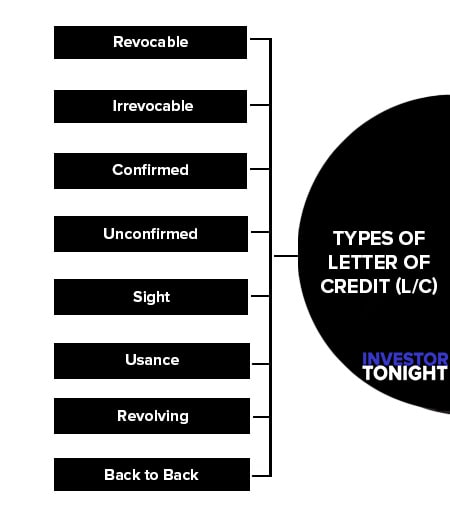

Types of Letter of Credit (L/C)

- Revocable Letter of Credit

- Irrevocable Letter of Credit

- Confirmed Letter of Credit

- Unconfirmed Letter of Credit

- Sight Letter of Credit

- Usance/Time Letter of Credit

- Revolving Letter of Credit

- Back to Back Letter of Credit

Revocable Letter of Credit

A revocable L/C may be cancelled or modified without the permission of or notice to the exporter/beneficiary by the issuing bank and it is seldom used.

Irrevocable Letter of Credit

It cannot be cancelled or amended without the beneficiary’s consent. An irrevocable L/C obligates the issuing bank to honor all drawings presented in conformity with the terms of the L/C.

Confirmed Letter of Credit

It is a special type of L/C in which confirming bank (generally a local bank in the exporter’s country) in addition to the issuing bank has added its guarantee by adding a clause, ‘The above credit is confirmed by us and we hereby undertake to honour the drafts drawn under this credit on a presentation provided that all terms and conditions of the credit are duly satisfied.’ Although the cost of confirming by two banks makes it costlier, this type of L/C is more beneficial for the beneficiary as it doubles the guarantee.

Unconfirmed Letter of Credit

Under it, the issuing bank asks the corresponding bank to advise about the L/C without any confirmation on its part. It mentions, ‘The credit is irrevocable on the part of the issuing bank but is not being confirmed by us.’

Sight Letter of Credit

It states that the payments would be made by the issuing bank at sight, on-demand or on presentation. The payment is made when documents are presented.

Usance/Time Letter of Credit

In case of usance/time credit, drafts are drawn on the issuing bank or the correspondent bank at specified usance period. The credit will show whether the usance draft are to be drawn on the issuing bank or in the case of confirmed credit on the confirming bank. The payment is made at a future fixed time from presentation of documents (e.g. 60 days after sight).

Revolving Letter of Credit

Under it, the amount involved is reinstated when used, i.e. the amount becomes available again without issuing another L/C and usually under the same terms and conditions.

Back to Back Letter of Credit

It is issued when exporter uses them as a cover for opening a credit in favour of the local suppliers. As the credits are intended to cover same goods, it should be ensured that the terms are similar except that the price is lower and validity earlier.

Advantages of Letter of Credit

Advantages to the Importer

- Importer is assured that the exporter will be paid only if all terms and conditions of the L/C have been met.

- Importer is able to negotiate more favourable trade terms with the exporter when payment by L/C is offered.

Disadvantages to the Importer

- A L/C does not offer protection to the importer against the exporter shipping inferior quality goods and/or a lesser quantity of goods. Therefore, it is important that the importer conduct the suitable due diligence to measure the goodwill of the exporter. If the exporter acts fraudulently, the only recourse available to the importer is through legal proceedings.

Note: Added protection to the Importer may be provided by requesting additional documentation in the Letter of Credit, e.g. a Certificate of Inspection. - It is necessary for the importer to have a line of credit with a bank before the bank is able to issue a L/C. The amount outstanding under each L/C issued is applied against this line of credit from the date of issuance until final payment.

Advantages to the Exporter

- The risk of payment depends upon the creditworthiness of the issuing Bank and the political risk of the issuing bank’s domicile, and not the creditworthiness of the importer.

- Exporter agrees in advance to all requirements for payment under the L/C. If L/C is not issued as agreed, the exporter is not obligated to ship against it.

- Exporter can further reduce foreign political and bank credit risk by requesting confirmation of the L/C by another bank.

Disadvantages to the Exporter

- Documents must be prepared and presented in strict compliance with the requirements stipulated in the L/C.

- Some importers may not be able to open L/C due to the lack of credit facilities with their bank which consequently shows export growth.