Hedging refers to a technique to transfer the risk. It is used to avoid any worsening of an exchange position; an importer can hedge an international transaction by trading in the foreign exchange market.

By entering the foreign exchange market, one can eliminate the uncertainty regarding the price that would have to be paid to acquire the needed foreign currency.

The objective of hedging or risk management is to transfer risk from one individual or corporation to another individual or corporation. The person off-loading the risk is the hedger; the person taking on the risk is the speculator or trader.

The hedger is concerned with adverse movements in security prices or with increase in volatility, which increase the overall riskiness of his position.

Table of Contents

For example: If an individual has long position (net assets position) in cash market securities, he will be concerned about the prices of those securities falling and will want to protect against this possibility.

Alternatively, if an individual has a short position (net liability position) in cash market securities, he will be concerned about rising prices and will want to protect against this possibility.

In order to hedge successfully and so transfer all risk, the hedger will have to select a suitable hedging instrument among the give below.

Hedging Instruments

Forward exchange cover

Forward exchange cover is created to hedge foreign currency loans taken by companies. RBI has permitted authorized dealers, who can book forward cover on a roll-over basis as necessitated by the maturity dates of the underlying transaction market condition and the need to reduce costs to the customer.

Where the foreign currency amount to be covered cannot be precisely quantified, as in the case of interest payable on loans contracted on a floating rate basis, authorized dealers will book forward contracts for an amount arrived at on the basis of reasonable estimate. Small amounts of shortfalls or excess will be purchased or sold on a spot basis.

Forward interest rates cover

It offers an opportunity to lock in for a future date and interest rates in a volatile rate environment. This enables borrowers to fix interest rates on existing floating rate debt or set a rate today for a debt to be taken in future.

The difference between actual rate on the date of the interest roll over and contracted rate is settled between the client and the bank. Borrowers use an interest rate forward to protect themselves from a rise in interest rates.

Hedging Strategies

- Currency Swap

- Interest Rate Swap

- Currency Futures and Currency Options

- Hedging in Currency Future Markets

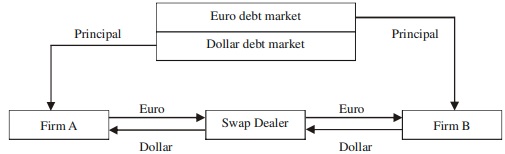

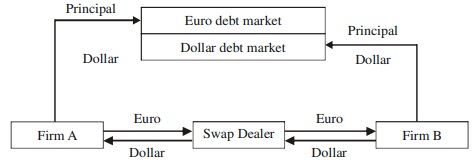

Currency Swap

A currency swap is an agreement to exchange fixed or floating rate payments, in one currency for fixed or floating payments in a second currency plus an exchange of the principal currency amounts. A currency swap may include the following three stages:

- A spot exchange of principal, which forms part of the swap agreement as a similar effect can be obtained by using the spot foreign exchange market.

- Re-exchange of principal on maturity.

- Continuity exchange of interest payments during the term of the swap, which represents a series of forward foreign exchange contracts during the term of the swap contract.

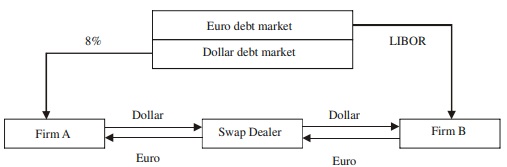

For example: Firm ‘A’ can borrow EURO at a fixed rate of 8 percent or it can borrow USD at a floating rate of 1 year LIBOR. Firm ‘B’ can borrow at a fixed rate of 9.2 percent and can borrow USD at 1 year LIBOR. If Firm ’B’ needs fixed rate EURO, it will approach the swap dealer, provided Firm ‘A’ needs floating rate USD.

Step 1: Firm A borrows Euro at 8.0% interest rate and Firm B borrows US dollar at LIBOR.

Step 2: The two firms exchange the borrowed currencies with the help of swap dealer. After the exchange, Firm A will have US dollar and Firm B will have Euro

Step 3:

Interest payment will flow. Firm A will pay LIBOR on US dollar that will reach the US dollar market through the swap dealer and then through Firm B. Similarly, Firm B will pay a fixed rate of interest which will flow to the fixed rate Euro market through the swap dealer and through Firm A.

Firm B will pay a fixed rate of interest to the swap dealer that will be more than 8.0% but less than 9.20%. The swap dealer will take its own commission and shall pay to Firm A.

Step 4: Two principals will be exchanged between two counter-parties. Firm A gets back Euro and repays it to the lender. Firm B gets back US dollar and repays it to the lender.

Interest Rate Swap

Interest Rate Swap It is an arrangement whereby one party exchanges one set of interest rate payments for another. The most common arrangement is an exchange of fixed interest rate payment for another rate of over a period of time.

Features of Interest Rate Swap

- Principal value upon which the interest rate is to be applied

- Fixed interest rate to be exchanged for another

- Formula type of index is used to determine the flowing rate

- Frequency of payment is agreed upon

- Life time of swap

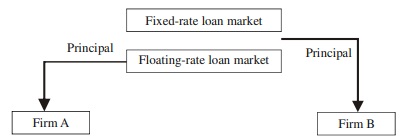

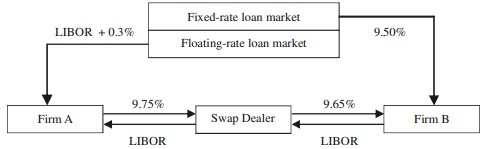

Example: Let firm A need a fixed-rate loan, which is available at a rate of 10.50% to be computed half yearly but it has access to a cheaper rate fund available to it at LIBOR + 0.3%. Firm B needs floating rate funds for 6 months LIBOR flat but it has access to cheaper fixed-rate funds available to it at a rate of 9.5%, to be computed half yearly.

Both the principals are identical in size and maturity and in the same currency, the interest rate swap will occur in the following steps.

Step 1: If Firm A has access to floating-rate loan market, it will borrow from floating rate market and Firm B having access to fixed loan market will borrow the fixed loan.

Step 2: Since both firms have not borrowed according to their needs, they approach a swap dealer. Firm A needs fixed rate loan, so the swap dealer asks Firm A to pay fixed rate interest to him as if Firm A has borrowed a fixed rate loan.

The fixed rate of interest payable through the swap dealer is higher than what Firm B has to pay to the lender in the fixed rate loan market but lower than what Firm A has to pay to the lender, if it had borrowed from the fixed rate loan market. In exchange, the swap dealer pays Firm A the interest at 6 month LIBOR.

Firm A pays LIBOR+0.3% to the lender on its floating rate borrowing.

The swap dealer asks Firm B to pay 6 month LIBOR as if it has borrowed floating rate loan. In exchange, the swap dealer pays Firm B fixed rate of interest which is higher than what Firm B has to pay to its lender. This is the interest rate that the swap dealer has received from Firm A minus its own commission.

Step 3: At maturity, the two firms repay the loan. Firm A repays the floating rate loan and Firm B repays the fixed rate loan.

Cost of Swap

While there is no exchange risk involved in swap transactions, there is a cost involved. The swap cost depends on the currency being in premium or discount in the forward market.

A currency is said to be at premium against the other currency if it is costlier in the forward and it is said to be at a discount against the other currency if it is cheaper in the forward.

Currency Futures and Currency Options

Currency future is a future contract to exchange one currency for another at a specified date in the future at a price that is fixed on the purchase date. Currency futures were first created in 1970 at the International Commercial Exchange in New York.

Currency options are basically rights given to the buyers of foreign currency to buy or sell a specific amount of foreign currency at a specific exchange rate (the strike price) till a specific date when the contract expires. Currency options may be entered either for a put or call.

A put option gives the right to sell a foreign currency whereas a call option gives a right to buy foreign exchange. This depends upon the position that is required under a specific situation by the party entering into an options market. A put option is required when the party requires foreign exchange.

By buying a put option the party sells the domestic exchange to procure the right amount of foreign exchange a specified rate. The reverse is done, when payment is needed to the done by the party. A call option is entered so that foreign exchange can be bought by exchanging the domestic currency.

Leads, Lags and Netting

A firm having exposures to pay foreign currency can make payments in advance prior to due date called ‘Leads’ in order to take advantage of a lesser rate of foreign currency. In such cases, the firm should consider the interest loss on an opportunity to deploy funds elsewhere.

If the firm delays the payments over the due date to take advantage of the exchange fluctuation it is called ‘Lags.’ The technique used in this is to delay payment of weak currencies and bring forward payment of strong currencies.

Netting is a concept of setting up the net amounts owned or amounts as a result of trade within the firm, i.e., between MNC parent company and its subsidiaries. The basic idea behind netting is to transfer only net amounts, usually within a short period.

Instead of making each payment—incurring transaction costs—the net position between the two companies can be ascertained say, every three months and one payment only to be made by the company which is in the net debtor position.

Similarly, a concept in line of netting is matching receipts and payments. The foreign exchange rate risk can be eliminated or reduced, if the company which is having exposure to receipts and payments in the same currency. The company can offset its payments against its receipts if it can plan properly. This can be managed by operating a bank account overseas to offset the transactions.

Hedging in Currency Future Markets

Futures contracts are an effective means of managing risks. Using futures to offset or reduce existing risks is called hedging. Banks use interest rate futures to hedge the risk arising from their asset-liability mismatch. Banks have to fund long-term assets such as mortgage loans with short-term liabilities such as savings and demand deposits.

This gives rise to the asset-liability mismatch. Similarly, stock index futures are used by portfolio managers to manage the risk of their stock portfolios. Importers, exporters and multinational corporations use foreign currency futures to manage the foreign exchange risk.

Hedging with Futures

Hedging refers to a transaction on a futures exchange undertaken to reduce a preexisting risk inherent in an underlying business activity. Depending on the risk being hedged and the construction of the hedge, futures hedges can be classified as follows.

- Short hedge: A short hedge is used by a firm that expects to sell an asset in the future. The firm takes a short futures position to hedge the price of the asset.

- Long hedge: A long hedge is used by a firm that expects to buy an asset in the future. The firm takes a long futures position to hedge the price of the asset.

- Inventory hedge: An inventory hedge involves establishing a futures position to hedge an existing position in the cash market. Inventory hedges are generally established in commodity markets.

- Anticipatory hedge: An anticipatory hedge involves establishing a futures position to hedge a cash position that may be taken in future. Anticipatory hedges are generally established in financial markets.

- Micro hedge: A micro hedge is a futures position that is matched against a specific asset or liability item on the balance sheet (e.g., a company hedging a foreign currency loan to be repaid in the next six months).

- Macro hedge: A macro hedge is a futures position designed to hedge the combined risk of many assets and liabilities (e.g., a multinational corporation using currency futures to hedge the currency risk of its net receipts/ payments, i.e., receipts minus payments of different currencies.

- Strip hedge: A strip hedge involves establishing a series of futures contracts maturing at successively longer periods. Such a hedge is used to cover the risk of a sequence of payments such as those in a long-term swap arrangement.

- Stack hedge: A stack hedge is also used to cover the risk of a sequence of payments over a long period of time.

However, instead of entering into a number of contracts, the entire futures position is established or stacked in the front month.

The initial position minus the portion of the hedge that is no longer needed is then rolled forward to the next period contract.